The U.S. government borrowed $1 trillion in just the first five months of fiscal year 2026. Not the full year — five months. By October, that number will likely reach $1.9 trillion, adding to a national debt already north of $36 trillion. Politicians debate it endlessly. Most Americans tune it out. That’s a mistake — because the debt is no longer an abstract fiscal concept. It is actively shaping your mortgage rate, your tax bill, the cost of federal programs you depend on, and the long-term growth trajectory of the economy you live in.

The question isn’t whether the debt is large. It clearly is. The question is: at what point does it start costing you money in ways you can actually feel — and are we already there?

The Big Picture: How Did We Get Here?

The U.S. has run a deficit in most years since 2001. But the scale accelerated sharply through the COVID-19 pandemic, the 2021 and 2022 stimulus packages, and then the 2025 One Big Beautiful Bill Act (OBBBA), which cut taxes and increased defense and border spending simultaneously.

Fact: Federal debt held by the public stands at nearly $31 trillion today and is projected to grow to $56 trillion by 2036 — a $25 trillion increase in one decade. As a share of the economy, debt will grow from 100% of GDP today to a record 108% by 2030 and 120% by 2036, according to the Congressional Budget Office’s February 2026 Budget and Economic Outlook.

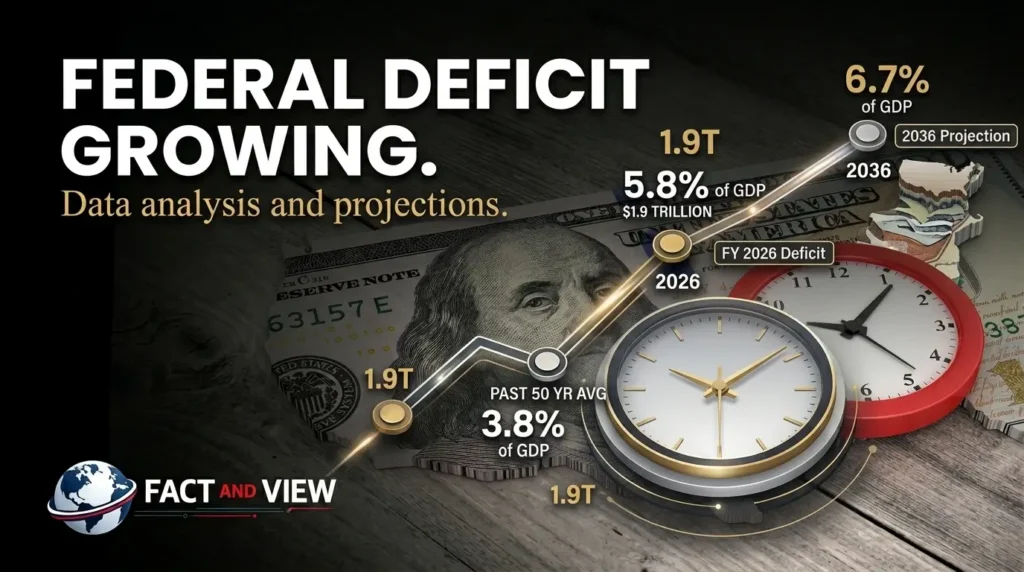

Fact: The federal deficit in fiscal year 2026 is $1.9 trillion — 5.8% of GDP. That compares to the 3.8% average over the past 50 years. Deficits are projected to grow to 6.7% of GDP by 2036.

Fact: Under CBO’s long-term projections, the national debt will rise to 175% of GDP by 2056, or roughly $168 trillion in nominal terms. Total deficits will average 7.1% of GDP over the next three decades.

To put that in perspective: the only time U.S. debt approached today’s levels relative to GDP was immediately after World War II — when it peaked at 106% of GDP. At that point, the U.S. was the world’s dominant industrial power with decades of growth ahead to grow out of it. The fiscal arithmetic today is structurally different.

The View: The debt has crossed a threshold where it’s no longer a future risk — it’s a present one. We have moved from “someday this will be a problem” to “this is already changing behavior in the bond market, at the Fed, and in the government’s ability to respond to the next crisis.” The debate is no longer about whether the debt matters; it’s about how fast the consequences arrive.

Deep Dive: Four Ways the Debt Is Already Affecting You

1. Interest Payments Are Crowding Out Everything Else

This is the most immediate and underappreciated consequence of the debt. The federal government now spends more on interest than on the entire defense budget.

Fact: Net interest payments on the national debt will more than double over the next decade, rising from $1.0 trillion in FY 2026 to $2.1 trillion by FY 2036. Interest payments are projected to rise from about 14% of total federal spending in FY 2026 to nearly 19% by FY 2036.

Every dollar sent to bondholders is a dollar unavailable for infrastructure, education, research, defense readiness, or disaster response. This isn’t a political argument — it’s arithmetic. When interest costs consume an ever-larger share of the budget, the government’s ability to invest in productive capacity declines. That directly affects long-term growth — and your future income.

The View: The crowding-out effect is already constraining policy. A Committee for a Responsible Federal Budget analysis shows that the average interest rate paid on the national debt could exceed the economic growth rate starting in FY 2031. If that occurs on a sustained basis, the U.S. risks a debt spiral — when interest costs increase interest rates and depress growth, and depressed growth further increases interest costs — absent significant fiscal reforms. That’s not alarmism. That’s the CBO’s own scenario analysis.

2. Higher Treasury Yields Keep Mortgage Rates Elevated

Here’s the direct line from Washington’s borrowing to your monthly payment. The government finances its deficit by issuing Treasury bonds. The more bonds it issues, the more it must offer to attract buyers — meaning yields rise. And since mortgage rates are priced off the 10-year Treasury yield, more government borrowing translates directly into higher borrowing costs for households.

Fact: Treasury yields have been trending higher since the onset of the Middle East conflict, driven by concerns that elevated energy prices could reignite inflation and force major central banks to keep rates higher for longer. The 10-year Treasury yield tested nine-month highs above 4.45% in late April 2026, before easing to around 4.32–4.35%.

Fact: The average 30-year fixed mortgage rate currently stands at approximately 6.4%, well above the historic lows of 2021. Freddie Mac’s latest 30-year average came in at 6.3%.

Charles Schwab’s 2026 fixed income outlook notes that the prospect of increasing supply of bonds is likely to keep long-term yields elevated despite Fed policy easing. Ten-year Treasury yields may not fall much below 3.75% even if the Fed cuts rates, with risk they move back toward 4.5% at times.

The View: This is the hidden tax of the national debt on every American with a mortgage, a car loan, or a student loan. The structural upward pressure on Treasury yields from deficit financing means the Fed’s ability to ease borrowing conditions — even when inflation allows — is partially offset by the sheer volume of new government bond issuance. Rate relief is slower, smaller, and shorter than it would be in a lower-debt environment.

3. Weak Treasury Auctions Are Flashing a Warning Signal

Bond markets are not abstract. When demand for U.S. Treasuries weakens, yields rise — because the government must offer higher returns to attract buyers. In March 2026, that warning signal started flashing.

Fact: A series of weak Treasury auctions in March added to concerns about weakening demand for a growing supply of federal debt. Primary dealers took 24% of a 2-year note auction in late March, roughly twice the share normally absorbed by these dealers, with 5- and 7-year securities also seeing weak demand. Primary dealers are the buyers of last resort — when they’re absorbing twice their normal share, it means the rest of the market didn’t show up.

This is not a crisis signal — yet. But it is a structural warning about what happens as deficits grow and the supply of Treasuries expands faster than global investor appetite.

The View: Weak auctions are the bond market’s equivalent of a check-engine light. They don’t tell you the engine has failed — they tell you something is wrong and getting worse. In a world where the U.S. needs to sell trillions in new debt every year, sustained weak demand means persistently higher yields, which means higher costs across the entire economy’s borrowing stack.

4. Reduced Fiscal Space for the Next Crisis

Here is perhaps the least-discussed consequence: the debt erodes the government’s ability to respond to the next economic shock. The fiscal firepower that allowed for $5 trillion in COVID relief in 2020 came at a cost. Replicating that response today — with debt at 101% of GDP and interest payments already at record levels — would be dramatically more difficult.

Fact: High and rising debt levels present significant risks to the economy, including slower economic growth, higher interest rates, increased inflationary pressure, heightened national security risks, reduced fiscal space, and greater risk of a fiscal crisis, per the Committee for a Responsible Federal Budget’s analysis of CBO’s February 2026 baseline.

The View: When the next recession arrives — and one always does — the U.S. will face a stark choice: borrow more at elevated yields to stimulate growth, accept a deeper downturn without fiscal response, or cut spending in ways that hit Social Security and Medicare. None of those options is painless. All of them trace back to the structural deficit path the country is currently on.

Risks & Opportunities: Three Scenarios

Base Case (~55% probability): Slow Burn

Deficits remain above $1.9 trillion annually. Debt grows as a share of GDP but no acute crisis materializes in the near term. Interest payments consume an increasing share of the budget. Growth continues at 1.8–2.2%. The Fed holds rates steady; mortgage rates stay in the 6.0–6.5% range. No major fiscal reform before the 2028 presidential election.

What this means for you: Mortgage relief is slow and limited. Federal programs face quiet erosion as interest crowds out discretionary spending. Your long-term investment returns are modestly lower than they would be in a lower-debt environment.

Upside Scenario (~20% probability): Growth and Reform

AI-driven productivity acceleration pushes GDP growth above 2.5% sustainably. Higher growth generates higher tax revenues, automatically reducing the deficit-to-GDP ratio without spending cuts. A bipartisan fiscal deal — triggered by pressure from bond markets — combines modest tax increases and entitlement reforms to stabilize the debt trajectory.

What this means for you: Mortgage rates ease toward 5.5–6% by 2027. Federal programs are stabilized. Higher growth means real wage gains that outpace borrowing costs. This scenario requires political will that hasn’t been visible recently — but it’s not impossible.

Downside Scenario (~25% probability): Bond Market Pressure

A sustained loss of appetite for U.S. Treasuries — driven by geopolitical shifts, foreign central bank reallocation, or continued weak auctions — forces yields significantly higher. The 10-year Treasury moves above 5%, pushing mortgage rates back toward 7–8%. The Fed is caught between controlling inflation and defending financial stability. A fiscal crisis or forced austerity becomes the base case.

What this means for you: Mortgage rates spike to levels not seen since the early 1980s. Business investment contracts as capital costs rise. Federal spending cuts land hardest on discretionary programs — education, infrastructure, research. Growth slows sharply.

Fact: CBO projects annual budget deficits will average 6.1% of GDP over the next decade — twice the 3% of GDP deficit target that economists broadly consider necessary to put the debt on a sustainable path. Without policy change, the downside scenario becomes structurally more likely with every passing year.

The Bottom Line

Should you be worried? Yes — but in a calibrated way. The debt is not a ticking clock with a known deadline. Countries can carry high debt loads for extended periods. Japan’s debt exceeds 260% of GDP and has not collapsed. But Japan has the world’s highest domestic savings rate to fund its deficits internally. The U.S. depends on foreign buyers. That’s a structural difference that matters.

For consumers: The debt’s most direct current impact is on your borrowing costs. Persistently elevated Treasury yields — driven partly by the government’s voracious borrowing — are keeping mortgage rates, auto loan rates, and credit card rates higher than they would otherwise be. If you have variable-rate debt, pay it down. If you’re waiting to buy a home at lower rates, Charles Schwab’s 2026 outlook suggests ten-year Treasury yields may not fall much below 3.75% — meaning 30-year mortgage rates may not sustainably return below 5.5–6% in this environment.

For investors: The crowding-out effect on private investment is a long-term headwind for equity valuations, particularly in capital-intensive sectors. Treasury Inflation-Protected Securities (TIPS) offer real yields of 1.25–2.0% — a structurally attractive hedge in a high-debt, persistent-inflation environment. Municipal bonds remain efficient for investors in higher tax brackets.

For business owners: The fiscal path raises two near-term planning risks. First, tax policy uncertainty — with current provisions set to expire or change, modeled tax scenarios for 2027 and 2028 now span a wider range than at any point in recent history. Second, government contract and program continuity — businesses that depend on federal spending should build contingency plans for a discretionary spending squeeze driven by interest costs.

The core conclusion. The national debt isn’t a problem for some future generation to solve. Its consequences — elevated borrowing costs, constrained fiscal space, weakening demand for Treasuries — are arriving now. The debt doesn’t have to cause a crisis to cost you money. It already does.

Sources: CBO Budget and Economic Outlook, February 2026 · CBO Long-Term Budget Projections · Committee for a Responsible Federal Budget · CRFB Deficit Tracker · Charles Schwab Fixed Income Outlook 2026 · Bankrate — Fed and Mortgage Rates · U.S. Treasury Interest Rate Statistics · TradingEconomics — 10-Year Treasury Yield · American Action Forum — CBO Outlook Analysis

© Fact and View, 2026. For informational purposes only. Not investment advice.

Be First to Comment