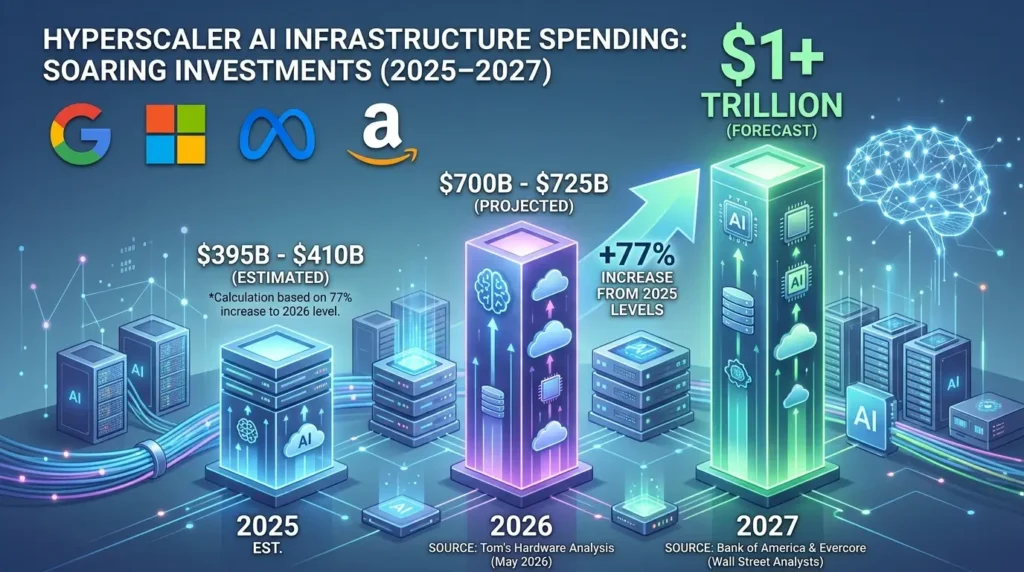

The five largest U.S. technology companies — Microsoft, Alphabet, Amazon, Meta, and Oracle — have collectively committed between $700 billion and $725 billion in capital expenditure for 2026. That is nearly double their 2025 spending. They are building data centers so large that they’ve signed long-term nuclear energy agreements to power them. Google Cloud’s contract backlog just hit $460 billion — roughly double what it was three months ago. Amazon expects negative free cash flow of $17–$28 billion this year. They are doing this anyway.

When the world’s most sophisticated capital allocators are spending at this velocity with this level of conviction, the question “is it too late to invest in AI stocks?” deserves a specific, data-driven answer — not a general observation about how much the sector has already run.

The answer is nuanced. For some AI stocks: no, it is not too late. For others: you are paying for perfection and may not get it. The distinction between the two categories is the most valuable analytical judgment you can apply to your portfolio in May 2026.

The Big Picture: The $700 Billion Infrastructure Super-Cycle

The AI investment cycle is not a narrative. It is a capital commitment of historic scale — and the commitment is accelerating, not plateauing.

Fact: The four hyperscalers — Alphabet, Microsoft, Meta, and Amazon — plan to spend $700–$725 billion combined on AI infrastructure in 2026, up 77% from 2025 levels, per Tom’s Hardware’s May 2026 analysis. Wall Street analysts at Bank of America and Evercore now project combined AI capex exceeding $1 trillion in 2027.

Fact: Google Cloud’s contract backlog reached $460 billion — roughly double its $240 billion figure from Q4 2025. Microsoft has an $80 billion Azure backlog it cannot fulfill due to power constraints. Approximately 40% of announced AI data center projects face construction delays — not from chip shortages, but from electricity grid bottlenecks, per NextWaves Insight’s infrastructure analysis.

Fact: Data center power demand from AI is projected to reach 1,000 TWh globally by 2026 — equivalent to Germany’s entire electricity consumption. Microsoft has signed a 20-year nuclear power purchase agreement with Constellation Energy to restart Three Mile Island specifically for AI data center load.

The View: When demand so dramatically outpaces supply that Microsoft is restarting nuclear power plants to keep up, we are not in the speculative early phase of an AI cycle. We are in its industrial buildout phase — the equivalent of the 1990s fiber optic cable laying, except the infrastructure being deployed is generating immediate, measurable revenue. Google Cloud’s $460 billion backlog is not hope. It is signed contracts. That changes the investment thesis fundamentally — this is not 1999 speculation; it is 2026 infrastructure monetization.

Related reading: Where Smart Money Is Moving Right Now (2026 Update) — how institutional capital is positioning across the AI infrastructure value chain.

Deep Dive: Five Categories of AI Stocks — and Where the Value Lies Now

1. Semiconductor Leaders: The Picks-and-Shovels Play

Nvidia remains the most direct expression of the AI infrastructure buildout — and paradoxically, one of the more reasonably valued ways to access it.

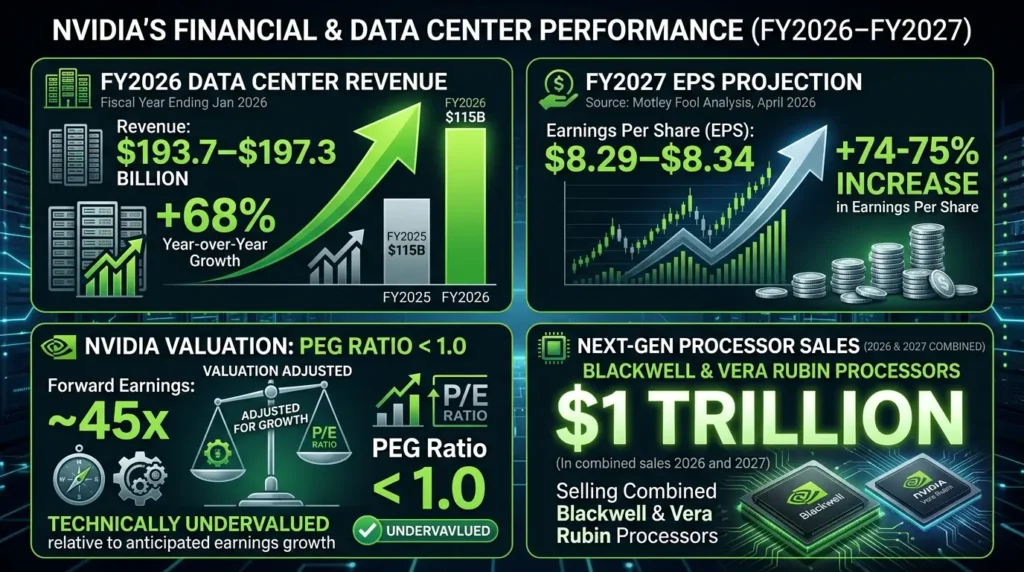

Fact: Nvidia’s data center segment generated $193.7–$197.3 billion in FY2026 revenue (fiscal year ending January 2026), up 68% year-over-year. Analysts project a 74–75% increase in earnings per share to $8.29–$8.34 for FY2027, per Motley Fool’s April 2026 analysis. At approximately 45 times forward earnings, Nvidia’s PEG ratio — which adjusts valuation for growth — sits below 1.0, indicating it is technically undervalued relative to its anticipated earnings growth. Nvidia expects to sell $1 trillion worth of its Blackwell and Vera Rubin processors in 2026 and 2027 combined.

Fact: The Global X Artificial Intelligence & Technology ETF is down approximately 3% year-to-date in 2026 — a pullback driven by broader market volatility, not deteriorating AI fundamentals. Nvidia itself was down as much as 12% in late March before recovering. As of May 14, 2026, Nvidia is up 15% year-to-date.

Fact: AMD has significantly outperformed Nvidia on the market in 2026. But Nvidia’s PEG ratio remains more favorable than AMD’s, per Motley Fool’s May 17 comparative analysis. Gartner estimates the global semiconductor industry’s revenue could increase 64% in 2026 to $1.32 trillion — powered by AI processor and networking demand.

The View: The “too late to buy Nvidia” question was being asked when the stock was at $400 in 2023. It was at $800 in 2024. The question is structural, not temporal. A company with $1 trillion in forward hardware commitments, 75% projected earnings growth, and a PEG ratio below 1.0 is not prohibitively expensive — it is the rare large-cap growth stock where the valuation is arguably supported by the earnings trajectory. The risk is execution: if data center demand softens or a competing architecture gains traction, multiple compression would be severe.

2. Cloud Hyperscalers: The Revenue Capture Layer

The hyperscalers — Microsoft, Alphabet, Amazon — are both the largest buyers of AI infrastructure and the companies monetizing it through cloud services. They are spending $700 billion to capture what they believe will be far more in future revenue.

Fact: Microsoft’s Azure cloud grew 26% in Q4 2025. Google Cloud grew 48% in the same period, with a $460 billion backlog. Jefferies analysts stated: “Cap-ex keeps climbing, but ROI is evident via ~$2 trillion backlog and accelerating cloud growth. Margin leverage holds for the hyperscalers despite AI investments.” Microsoft is tracking toward $190 billion in 2026 capex — 24% above analyst estimates — with the CFO stating the company expects to remain capacity-constrained through at least the end of 2026.

Fact: Morningstar’s May 8, 2026 best AI stocks analysis identified Microsoft as currently trading 31% below its $600 fair value estimate — making it the most undervalued mega-cap AI stock by conventional valuation metrics, per Morningstar’s analysis.

The View: The hyperscalers present a paradox. Their free cash flow is being crushed by capex — Amazon faces negative FCF of $17–$28 billion in 2026; Meta’s FCF drops 90%. But their cloud backlogs are exploding. Investors who focus on near-term FCF compression miss the forward revenue story; investors who ignore FCF compression miss the near-term earnings risk. The right frame: Microsoft and Alphabet are long-duration compounders, not short-term trades. At Morningstar’s 31% undervaluation for Microsoft, the long-duration case is compelling for patient capital.

3. AI Infrastructure Enablers: The Overlooked Value Chain

Beyond the headline names, the AI buildout has created structural demand across an entire supply chain that most retail investors underweight.

Fact: The binding constraint on AI data center expansion is no longer chips — it is electricity. Approximately 40% of announced AI data center projects face delays due to power infrastructure bottlenecks. This creates structural demand for:

- Power utilities and nuclear operators — Constellation Energy (CEG) signed the Three Mile Island deal with Microsoft; Vistra, NRG Energy, and NextEra are all adding AI-specific power capacity

- Cooling technology — data center thermal management has become a $20B+ market; Vertiv Holdings (VRT) is the dominant pure-play

- Networking equipment — Broadcom (AVGO) has 99% of internet traffic touching at least one of its chips; Arista Networks powers hyperscaler spine networks

- Copper and rare earth materials — physical infrastructure of data centers requires enormous quantities; copper demand for AI data centers is projected to grow 200% by 2030

The View: The infrastructure enabler category is where the most underappreciated value sits in the AI investment landscape. When the narrative focuses on Nvidia and Microsoft, capital flows into the obvious names and away from the picks-and-shovels enablers. Vertiv, Constellation Energy, and Broadcom are each capturing durable, growing revenue streams from the AI buildout — at valuations that don’t carry the same “priced for perfection” risk as the hyperscalers.

Related reading: Best Investments During Inflation (2026 Guide) — including infrastructure REITs and data center exposure as inflation-protected AI plays.

4. AI Software and Applications: Where Monetization Is Just Beginning

Hardware and cloud infrastructure have captured the first wave of AI investment. Software — the layer where AI actually generates productivity and revenue for end users — is the next wave.

Fact: Dan Ives at Wedbush Securities has described 2026 as “the year AI spending must start showing ROI” — and the early enterprise software data is starting to validate that thesis. Salesforce AI agents are being deployed at scale. Microsoft Copilot seats are growing faster than any prior enterprise software product. Adobe’s AI creative tools are adding revenue per seat that wasn’t present in 2023.

The highest-quality AI software positions share three characteristics:

- Switching costs: Once an enterprise embeds an AI model in its workflow, displacement requires significant effort and risk

- Data network effects: Models trained on proprietary customer data become more accurate over time, creating compounding competitive advantage

- Pricing power: AI features command premium pricing that raises average revenue per user

The View: The AI software monetization wave is earlier-stage than the infrastructure buildout — which means higher upside potential and higher execution risk. The pure-play AI software companies (Palantir, C3.ai) carry extreme valuation multiples that require perfect execution. The more pragmatic approach: own the AI software opportunity through established platforms that are adding AI capability to existing customer bases — Microsoft, Salesforce, Adobe — rather than through speculative pure-plays.

5. DigitalOcean: The SMB AI Infrastructure Opportunity

One of the most interesting 2026 AI stock stories involves not the mega-caps but a company focused on small and medium-sized businesses.

Fact: DigitalOcean secured 60 megawatts of additional compute capacity and raised its 2026 revenue growth guidance to 26% — with acceleration to 50%+ projected for 2027 — before recently reporting earnings on May 5, 2026. The stock has climbed more than 50% since that earnings report, per Motley Fool’s May 14, 2026 analysis. At 81 times adjusted earnings, current valuation is stretched — a potential entry opportunity on a pullback.

The View: DigitalOcean’s AI thesis is that the hyperscalers’ products — built for enterprises with large IT departments and complex needs — are genuinely too complicated for the 100 million SMBs globally that need AI infrastructure without the enterprise complexity. If that thesis is correct and the 50% growth rate materializes in 2027, the current multiple looks reasonable in retrospect. At current prices, the risk-reward demands patience and position sizing discipline.

Risks & Opportunities: Three AI Stock Scenarios

Base Case (~50% probability): AI Capex Cycle Sustains, Sector Returns 15–25%

The $725 billion capex cycle continues. Cloud backlog data confirms ROI. Nvidia delivers on its $1 trillion Blackwell/Vera Rubin commitment. S&P 500 AI stocks return 15–25% in the second half as fundamentals reassert over geopolitical noise.

Positioning: Core holdings in Nvidia (NVDA), Microsoft (MSFT), Alphabet (GOOG), Broadcom (AVGO), Vertiv (VRT). Diversify through BOTZ (Global X Robotics & AI ETF) or AIQ (Global X AI & Technology ETF) for broad sector exposure.

Upside Scenario (~25% probability): AI Monetization Surprise, Multiple Expansion

Enterprise AI software adoption accelerates faster than consensus. Azure and Google Cloud revenue growth exceed 40%+ again in H2. Nvidia delivers earnings 20% above estimates. AI sector re-rates upward; Nvidia doubles from current levels.

Positioning: Increase Nvidia weight; add AI software exposure through Microsoft Copilot beneficiaries. This is the scenario where concentrated AI exposure pays off most dramatically.

Downside Scenario (~25% probability): Capex ROI Questions, Multiple Compression

A major hyperscaler guides revenue growth below 25%. FCF compression triggers analyst downgrades. The AI investment thesis gets stress-tested by investor impatience. AI stocks correct 20–35% as multiples contract toward historical norms.

Positioning: Reduce pure-play AI software exposure (highest multiple, most FCF-negative). Maintain infrastructure positions — Nvidia’s earnings trajectory protects it better than software from multiple compression. Add TIPS and gold as portfolio balance, per the inflation-hedging framework.

The Bottom Line

Is it too late to invest in AI stocks in 2026? For the right names, at the right size, with the right time horizon: no.

The AI infrastructure buildout is not speculative. It is a $725 billion capital commitment backed by $2 trillion in cloud backlogs, 75% projected earnings growth at the leading chipmaker, and nuclear power agreements that don’t get signed for hype. The ROI is beginning to show in cloud revenue growth rates. The structural demand is accelerating, not plateauing.

But the AI investment case in 2026 requires sector discipline that the 2020–2021 era didn’t demand:

Own the infrastructure, not just the narrative:

- Nvidia (NVDA) — PEG below 1.0, $1 trillion forward hardware commitment, 75% EPS growth

- Microsoft (MSFT) — 31% undervalued per Morningstar, Azure capacity-constrained, Copilot monetization accelerating

- Broadcom (AVGO) — networking infrastructure with AI-specific revenue streams, reasonable valuation

- Vertiv (VRT) — cooling and power infrastructure; benefits from 40% of data center projects delayed by power constraints

- Constellation Energy (CEG) — the nuclear power beneficiary of Microsoft’s Three Mile Island deal

Use ETFs for diversification:

- BOTZ — Global X Robotics & AI ETF for broad sector exposure

- SMH — VanEck Semiconductor ETF for chip sector concentration

- AIQ — Global X AI & Technology ETF for software-plus-hardware balance

Size appropriately. The downside scenario is real — a 20–35% correction from current AI stock levels is within historical norms for a sector trading at elevated multiples. Never allocate more than 15–20% of a total portfolio to a single thematic sector, regardless of conviction.

The AI revolution is not over. The infrastructure buildout is in its third year and accelerating. The monetization wave is just beginning. The question is not whether to invest — it is which part of the value chain offers the best risk-adjusted return from here.

Continue reading from Fact and View:

- Where Smart Money Is Moving Right Now (2026 Update) — the institutional allocation picture beyond AI

- Best Investments During Inflation (2026 Guide) — how to balance AI exposure with inflation protection in one portfolio

- Is the Stock Market Overvalued in 2026? Full Breakdown — the broader market context that governs AI stock valuation multiples

FAQ

Is it too late to buy Nvidia stock in 2026?

By fundamental metrics, no. Nvidia’s forward P/E of approximately 45 times earnings is supported by a PEG ratio below 1.0 — meaning the stock is technically undervalued relative to its anticipated 75% earnings growth rate. Nvidia’s data center revenue hit $193.7 billion in FY2026, up 68% year-over-year, with $1 trillion in forward commitments from Blackwell and Vera Rubin processor sales. The stock was down as much as 12% in late March 2026 before recovering to +15% year-to-date — suggesting the recent consolidation has created a more attractive entry than the January highs. As Motley Fool put it on May 8, 2026: “It isn’t too late for investors to buy Nvidia stock yet, as it could come out of its slump by delivering stellar quarterly reports.” Track Nvidia’s live price and analyst estimates at Nasdaq.

What is the best AI ETF to invest in 2026?

Three ETFs cover different parts of the AI value chain:

- BOTZ (Global X Robotics & AI ETF) — broad AI exposure including robotics, automation, and software; more balanced than semiconductor-only funds

- SMH (VanEck Semiconductor ETF) — concentration in chip companies; highest correlation to Nvidia and AMD performance; highest volatility

- AIQ (Global X AI & Technology ETF) — software-and-hardware balanced AI basket; down approximately 3% year-to-date in 2026 despite strong underlying fundamentals, creating a potential entry

For investors who want AI infrastructure exposure without single-stock risk, SMH for chips plus VNQ (REITs with data center exposure) plus XLE (energy for power demand tailwind) creates a diversified AI infrastructure portfolio without direct technology company concentration risk.

How much are Big Tech companies spending on AI in 2026?

The four hyperscalers — Alphabet, Amazon, Meta, and Microsoft — plan to spend $700–$725 billion combined on AI infrastructure in 2026, up 77% from 2025. Individually: Amazon ($200 billion), Alphabet ($185–$190 billion), Microsoft ($190 billion), Meta ($125–$145 billion). Wall Street analysts at Bank of America and Evercore project combined AI capex exceeding $1 trillion in 2027. The majority of this spending goes toward data center construction, GPU procurement, networking equipment, and energy infrastructure — not software development. Track the capex race at Statista’s Big Tech capex tracker.

Will AI stocks crash in 2026?

A 20–35% correction in specific AI names is possible — particularly in pure-play AI software companies trading at 80–100+ times earnings. But a broad AI crash comparable to the dot-com bust requires a fundamental collapse in demand — and the evidence points the opposite direction. Google Cloud’s $460 billion backlog (up 92% from one year ago), Microsoft’s capacity constraints, and Nvidia’s $1 trillion hardware commitment are not speculative indicators. They are demand confirmations. The risk scenario is multiple compression without fundamental collapse: stocks fall 20–30% not because the businesses are failing but because investors lose patience with near-term FCF compression from capex spending. That is a risk — but it is a valuation event, not a structural collapse.

Which AI stocks does Morningstar consider undervalued in 2026?

Morningstar’s May 8, 2026 analysis of the best AI stocks to buy identified companies in the AI index earning 4- or 5-star ratings — meaning they are undervalued relative to Morningstar’s fair value estimate. Microsoft is specifically highlighted as trading 31% below Morningstar’s $600 fair value estimate — making it the most undervalued mega-cap AI stock by this metric. Nvidia is also identified as attractively valued given its GPU dominance and CUDA software ecosystem. Read the full Morningstar analysis at morningstar.com/stocks/best-ai-stocks-buy-now.

What is the biggest risk to AI stocks in 2026?

The three most credible risks, in order of probability:

- FCF compression triggers analyst downgrades (~35% probability): Amazon faces negative FCF of $17–$28 billion in 2026; Meta’s FCF drops 90%. If revenue growth disappoints simultaneously, the “spend now, profit later” thesis gets stress-tested and multiples compress

- Geopolitical disruption to semiconductor supply chains (~25% probability): U.S.-China tensions over Taiwan directly threaten 92% of advanced semiconductor production; export controls on Nvidia chips to China have already reduced the addressable market

- Power infrastructure bottlenecks slow data center buildout (~20% probability): 40% of planned AI data centers face delays due to power constraints; if this extends timelines significantly, revenue recognition slips and growth rates disappoint

Related reading: Middle East Tensions Explained: What It Means for Oil Prices — energy supply disruptions directly affect AI data center operating costs and power availability.

Where can I track AI stock performance and industry data in real time?

Primary sources, all free:

- Morningstar AI Stock Ratings — updated fair value estimates and star ratings for major AI stocks

- Nvidia Investor Relations — earnings, guidance, and backlog data directly from the source

- Statista Big Tech Capex Tracker — quarterly hyperscaler spending comparison

- Futurum AI Capex Analysis — deep infrastructure spending breakdown

- FRED — Business Fixed Investment — macro context for technology capex within broader capital investment trends

- SEC EDGAR 13F Filings — track institutional AI stock holdings quarterly

Sources: Tom’s Hardware — Big Tech AI Spending $725B, May 2026 · CNBC — AI Capex Tops $1T in 2027, April 30, 2026 · CNBC — Tech AI Spending $700B, February 6, 2026 · Futurum — AI Capex 2026, February 12, 2026 · Motley Fool — Nvidia Still Buy, May 8, 2026 · Motley Fool — Nvidia vs. AMD May 17, 2026 · Motley Fool — Nvidia April 10, 2026 · Motley Fool — DigitalOcean May 14, 2026 · Morningstar — Best AI Stocks May 8, 2026 · NextWaves — Hyperscaler Capex 2026 · Fortune — $700B Spending No End in Sight, April 30, 2026

© Fact and View, 2026. For informational purposes only. Not investment advice.

Be First to Comment