The worst time to start investing is never. The second worst time is waiting for the “perfect” market conditions that don’t exist.

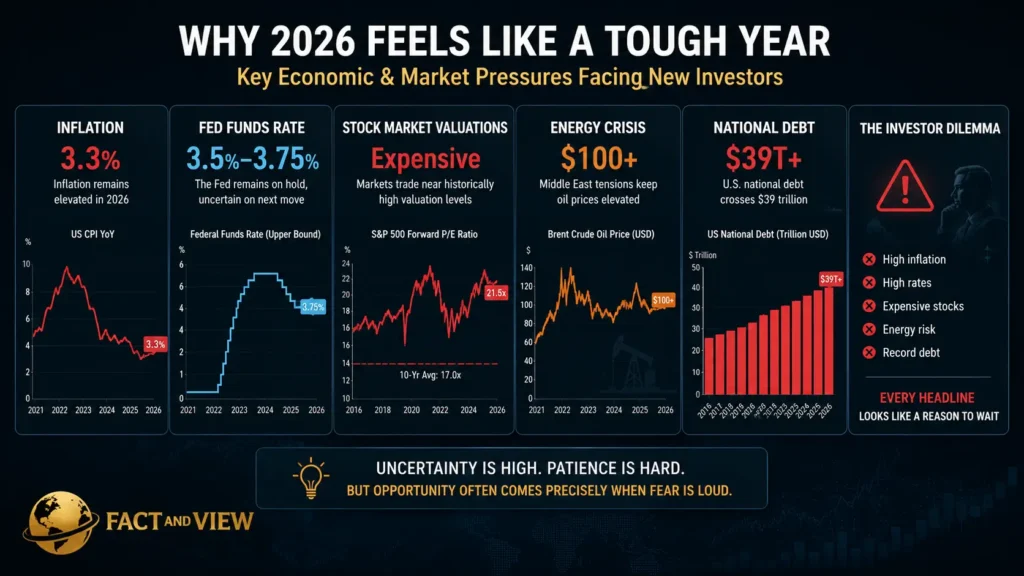

In 2026, most first-time investors face a legitimately difficult environment: inflation running at 3.3%, the Fed frozen at 3.5%–3.75%, the stock market trading at historically expensive valuations, a Middle East energy crisis keeping oil above $100, and a national debt crossing $39 trillion. Every headline looks like a reason to wait.

Here’s the problem with waiting: a 25-year-old who invests $200 per month at an average 10% annual return will accumulate $1.3 million by age 65. A 35-year-old who makes the same investment, also at 10%, will accumulate roughly $452,000 — a $848,000 difference for waiting one decade. That gap is not recoverable. No amount of smart market timing makes up for a decade of missing compound interest.

The question for a first-time investor in 2026 is not whether to start. It is how to build a strategy that survives this specific environment — geopolitical volatility, elevated valuations, sticky inflation, and elevated interest rates — while still capturing the long-run returns that make investing transformational.

This is that strategy.

The Big Picture: Why 2026 Is Actually a Good Time to Start

Counterintuitively, the complexity of 2026’s market environment works in a beginner’s favor in one critical way: it creates volatility, and volatility creates lower prices at regular intervals that dollar-cost averaging (DCA) is specifically designed to exploit.

Fact: Dollar-cost averaging ensures you buy more shares when prices are low and fewer when prices are high — naturally reducing your average cost over time. The Global X AI & Technology ETF is down approximately 3% year-to-date in 2026 despite strong underlying fundamentals. The S&P 500 delivered only 1% in the midterm election year of 2022 but recovered 15%+ in the following 12 months. Volatility is not the enemy of a beginner investor. It is the raw material for wealth accumulation through consistent, systematic investing.

Fact: More people are investing earlier than ever before in 2026. Fractional shares have lowered the barrier to entry, apps have removed friction, and information is everywhere. Fidelity, Schwab, and Vanguard all offer $0 commission trading. Fractional shares mean you can own a slice of Amazon or Nvidia for $5. The structural barriers to starting that existed 20 years ago — minimum account sizes, broker fees, information access — have essentially been eliminated.

The View: The paradox of the 2026 investing environment is that the same macro complexity that makes experienced investors nervous is largely irrelevant to a beginner’s 20–30 year wealth-building horizon. The Middle East conflict, the national debt, and the Fed’s rate decisions will all look like minor footnotes in 2046. What will matter is whether you started in 2026 or waited until 2028. Compound interest doesn’t negotiate with geopolitical risk.

Related reading: Best Investments During Inflation (2026 Guide) — once you’ve built your foundation, here’s how to inflation-proof the portfolio.

Deep Dive: The Six-Step Beginner Investing Framework for 2026

Step 1: Build Your Financial Foundation Before You Invest a Dollar

Investing without financial foundations is like building a house on sand. Two non-negotiables come first.

Emergency fund first. You need 3–6 months of living expenses in liquid savings — not invested in stocks — before you touch a brokerage account. Why? Because markets fall. A 20–30% market correction is normal and historically recurring. If you have no cash reserves and your car breaks down during a market downturn, you sell investments at the worst possible moment. Lock in 4.5%–5.0% APY in a high-yield savings account at Ally, Marcus, or SoFi while the rate environment holds.

Eliminate high-interest debt next. Credit card debt running at 20%+ APR delivers a guaranteed negative return that no investment can reliably beat. Paying off a $5,000 balance at 20% APR is the equivalent of earning 20% risk-free. The S&P 500 has never delivered a guaranteed 20% annual return. Your credit card balance does — in reverse. Eliminate it before investing a single dollar.

Related reading: Interest Rates Explained: How They Affect Your Money in 2026 — the full breakdown of why 20% credit card APR is the most destructive financial force in a typical household budget.

Step 2: Open the Right Accounts in the Right Order

Tax-advantaged accounts are the single most powerful legal tool available to beginner investors — and the most frequently ignored.

The priority order:

- 401(k) up to employer match — if your employer matches 3% of your salary, contribute at least 3%. That match is a guaranteed 100% instant return on that contribution. No investment beats free money.

- Roth IRA — the most powerful wealth-building account available to most Americans.

Fact: The Roth IRA contribution limit for 2026 is $7,500, with an additional $1,100 catch-up contribution for those aged 50 or older, bringing their limit to $8,600. Contributions are made with after-tax dollars, but all growth and qualified withdrawals in retirement are completely tax-free. For a 25-year-old investing $7,500/year in a Roth IRA at 10% average returns, the tax-free compounding over 40 years produces approximately $3.7 million — entirely tax-free at withdrawal. A traditional brokerage account generating the same returns would produce roughly $2.5 million after capital gains taxes.

- 401(k) beyond the match — after maxing the Roth IRA, return to your 401(k) for additional pre-tax contributions.

- Taxable brokerage — only after maxing tax-advantaged accounts. Use a taxable brokerage account after maxing out tax-advantaged accounts.

Best Roth IRA providers in 2026:

- Fidelity — zero expense ratio index funds, no account minimums, fractional shares

- Vanguard — the inventor of low-cost index investing, ideal for long-term buy-and-hold

- SoFi — received the highest mark on J.D. Power’s 2026 U.S. Investor Satisfaction Survey for DIY customer satisfaction; thousands of ETFs from $5

- Schwab — excellent research tools, zero commissions, fractional shares

Step 3: Start With Three Funds — Nothing More

The three-fund portfolio is the most battle-tested beginner investing framework in existence. It requires no stock-picking expertise, no market timing, and minimal ongoing management.

A simple, proven strategy: hold three funds — a US stock index fund, an international stock index fund, and a bond index fund. Adjust the percentages based on your age and risk tolerance.

The three funds:

- U.S. Total Market Index Fund — owns every publicly traded U.S. company. Options: VTI (Vanguard Total Stock Market ETF) or FZROX (Fidelity Zero Total Market Index, 0% expense ratio)

- International Stock Index Fund — owns large companies outside the U.S. across Europe, Asia, and emerging markets. Options: VXUS (Vanguard Total International Stock ETF) or FZILX (Fidelity Zero International Index, 0% expense ratio)

- Bond Index Fund — provides stability and income; reduces portfolio volatility during stock market downturns. Options: BND (Vanguard Total Bond Market ETF) or FXNAX (Fidelity US Bond Index)

Starting allocation by age:

- 20s–30s: 80–90% stocks (split 70/30 U.S./international), 10–20% bonds

- 40s: 70% stocks, 30% bonds

- 50s: 60% stocks, 40% bonds

- 60s+: 50% stocks, 50% bonds

In 2026 specifically, considering inflation running at 3.3%, a beginner might allocate 5–10% of the stock portion to an inflation hedge — an energy ETF (XLE) or a commodity fund (DBC) — without overcomplicating the core framework.

Step 4: Use Dollar-Cost Averaging — Systematically, Automatically

The most powerful behavioral tool in investing is removing behavior from the equation entirely.

Fact: Financial professionals prefer dollar-cost averaging for two reasons: it’s easy, and it takes the emotion out of investing. Dollar-cost averaging can help remove the impulse to time the market. Sean Pearson, CFP at Ameriprise Financial Services, is direct: “Dollar-cost averaging is a good, safe, tried-and-true way to do it.”

Set up automatic monthly transfers from your checking account to your investment account — the exact amount you’ve budgeted. The automation removes the weekly temptation to look at market headlines and decide this week is “not the right time.”

Starting capital by level:

- $100–$1,000: Start dollar-cost averaging weekly or monthly. Build a position in 2–3 index funds.

- $1,000–$10,000: Build the full three-fund portfolio. Max out IRA contributions if possible.

- $10,000+: Diversify across asset classes. Consider adding REITs, international exposure, and eventually individual stock positions in high-conviction names.

Step 5: Understand What You Actually Own

A three-fund portfolio isn’t three products. It’s a claim on the productive capacity of the global economy.

When you buy VTI, you own a fraction of approximately 3,800 U.S. companies — from Apple and Nvidia to regional banks and small manufacturers. When one company fails, the 3,799 others carry the portfolio. When the U.S. economy grows — which it has in 70 of the last 75 years — your investment grows with it.

Fact: The S&P 500 has never produced a negative 20-year rolling return in its history. In every 20-year period since 1900, holding a broad U.S. stock index has produced positive returns — through world wars, the Great Depression, the dot-com crash, the 2008 financial crisis, and COVID-19. That is the foundational data point that anchors every long-term investing strategy.

The volatility you see on a daily or annual basis is noise relative to this 20-year signal. The beginner investor’s primary job is not to pick the right stocks — it is to stay invested through the noise long enough for the signal to dominate.

Related reading: Is the Stock Market Overvalued in 2026? Full Breakdown — understanding current valuation context helps set realistic return expectations without derailing the core strategy.

Step 6: Add Inflation Protection in 2026 Specifically

The three-fund portfolio is evergreen. But 2026 has a specific condition — persistent inflation — that warrants one targeted adjustment for any investor starting today.

Fact: CPI ran at 3.3% in March 2026. Core PCE stood at 3.0% in February — above the Fed’s 2% target for the 24th consecutive month. The Middle East energy crisis has introduced upward pressure on food and fuel that has not yet fully worked through the inflation data. The IMF projects global inflation at 4.4% in its reference scenario.

For beginners starting a portfolio in this environment, add two inflation hedges to the core three-fund framework:

- I Bonds: $10,000 maximum per person at TreasuryDirect.gov — currently yielding 4.03%, zero credit risk, automatic CPI adjustment. This is your emergency fund complement, not your growth portfolio.

- TIPS via VTIP ETF — short-term TIPS ETF with lower duration risk than the full TIP fund, adding inflation protection to the bond allocation without sacrificing liquidity.

Related reading: What the Federal Reserve Really Does (Simple Explanation) — understanding how the Fed’s decisions connect to your savings account rates, mortgage costs, and investing environment.

Risks & Opportunities: Three Scenarios for a 2026 Beginner Investor

Base Case (~50% probability): Inflation Persists, Markets Deliver 5–8% in 2026

Inflation stays at 3–3.5%. The Fed holds rates. Markets deliver below-average returns — 5–8% for the year after pre-election volatility. A beginner who starts in 2026 and keeps buying through volatility lowers their average cost on every position.

What this means: Dollar-cost averaging works perfectly in this scenario. By year-end, a consistent investor will have bought at multiple price points, building a lower average cost than any one-time investor at peak prices.

Upside Scenario (~25% probability): Hormuz Reopens, Fed Cuts, Markets Rally 15%+

Iran diplomatic resolution eases energy prices. Inflation falls toward 2.5%. The Fed delivers two cuts. Markets rally 15%+ post-election, following the historical midterm pattern.

What this means: Beginners who stayed invested through the volatile spring enjoy the full recovery. Those who waited for “better conditions” buy in near the top. This is the classic scenario that makes waiting consistently worse than starting.

Downside Scenario (~25% probability): Stagflation Deepens, Markets Correct 20–30%

Middle East conflict escalates. Oil above $115. CPI spikes toward 5%+. Markets correct 20–30% as the Fed is forced to hold rates indefinitely.

What this means for a beginner: A 25-year-old experiencing a 30% market decline in year one of investing is not a financial disaster — it is a buying opportunity. The same $200/month buys 43% more shares at -30% prices. The only investors hurt by a correction are those who need the money now or sell in panic. A beginner with an emergency fund and no short-term liquidity need benefits from every price drop.

The Bottom Line

The beginner investor’s advantage in 2026 is time. Every experienced investor in the market today would trade their knowledge for another 20 years of compounding if they could. You have that advantage automatically — if you start.

Your six-step action checklist:

- ✅ Build a 3–6 month emergency fund in a high-yield savings account paying 4.5%–5.0%

- ✅ Pay off all credit card debt before investing anything else

- ✅ Open a Roth IRA at Fidelity, Vanguard, Schwab, or SoFi

- ✅ Contribute up to $7,500 ($8,600 if 50+) for 2026 — or start with whatever you can

- ✅ Buy VTI + VXUS + BND in age-appropriate proportions — automate monthly purchases

- ✅ Add $10,000 in I Bonds at TreasuryDirect.gov for inflation protection

The geopolitical complexity of 2026 is real. The Middle East war, the national debt, the Fed’s policy trap — these are genuine risks with genuine market implications. But none of them change the fundamental arithmetic of compound interest operating over 30 years. None of them should keep a 25-year-old from opening a Roth IRA today.

Start. Automate. Don’t look at it every day. Come back in 20 years.

Continue reading from Fact and View:

- Best Investments During Inflation (2026 Guide) — once the foundation is built, here’s the 2026-specific layer

- Is It Too Late to Invest in AI Stocks? — when you’re ready to move beyond index funds

- Where Smart Money Is Moving Right Now — the institutional playbook for the next 24 months

FAQ

How much money do I need to start investing in 2026?

Before investing, ensure you have an emergency fund of 3–6 months of expenses and have paid off high-interest debt like credit cards. Beyond that, you can start with as little as $1 — most major brokerages offer fractional shares with no minimums. Practically, $50–$100 per month is enough to build meaningful positions over time through dollar-cost averaging. The Roth IRA 2026 contribution limit is $7,500 annually, but you do not need to contribute that amount upfront. Contributing $625/month automatically gets you to the annual maximum.

What is a Roth IRA and why should beginners use it?

A Roth IRA is a retirement account where you contribute after-tax dollars. All growth inside the account — dividends, capital gains, price appreciation — compounds tax-free. Qualified withdrawals in retirement are completely tax-free. The 2026 Roth IRA contribution limit is $7,500, with an additional $1,100 catch-up contribution for those aged 50 or older, bringing the limit to $8,600. For most young investors in lower tax brackets today who expect to be in higher brackets at retirement, the Roth IRA is mathematically superior to the traditional IRA. Open one at Fidelity (fidelity.com) or Vanguard (vanguard.com) in under 15 minutes.

What is dollar-cost averaging and does it actually work?

Dollar-cost averaging (DCA) means investing a fixed amount of money on a regular schedule — weekly, bi-weekly, or monthly — regardless of what the market is doing. This strategy ensures you buy more shares when prices are low and fewer when prices are high — naturally reducing your average cost over time. The mathematical evidence for DCA is strong in volatile markets: it prevents the behavioral error of waiting for the “perfect” entry point that never reliably arrives, particularly for beginners who lack the experience to identify market turning points. Set up automated monthly contributions and the strategy runs on autopilot.

Should a beginner invest differently because of inflation in 2026?

The core three-fund strategy remains the foundation — but add two inflation-specific elements. First, purchase the annual maximum in I Bonds ($10,000 per person) at TreasuryDirect.gov — currently yielding 4.03% with automatic CPI adjustment. Second, replace your standard bond allocation with short-term TIPS via the VTIP ETF, which provides inflation protection within the bond portion of the portfolio. For the equity allocation, consider a 5–10% position in an energy ETF (XLE) as an inflation hedge within the stock allocation. These adjustments require one decision each and then run automatically — no active management needed.

Is 2026 a bad time to start investing because of market volatility?

No — and the data consistently shows the opposite. The S&P 500 has historically underperformed in midterm election years (averaging 1% returns) but then delivered average post-midterm 12-month returns of 15.1%. Pre-election volatility — concentrated in summer and fall 2026 — creates lower entry prices for systematic investors. A beginner who starts in 2026 and keeps investing monthly through the volatile pre-election period will own positions at prices that will look very attractive in retrospect by 2028. The investors hurt by volatility are those who need their money in the short term. Beginners with a 20–30 year horizon benefit from every market dip.

What’s the one financial mistake beginners make most often in 2026?

Waiting. The challenge in 2026’s investment environment is simply getting oriented — knowing what each option actually does, how risky it is, and how it fits into a bigger financial picture. Most beginners experience “analysis paralysis” — overwhelmed by options, waiting until they understand everything before starting anything. The compounding math is unforgiving: every year of delay has an exponentially increasing cost. A $7,500 Roth IRA contribution in 2026 that compounds at 10% for 40 years becomes approximately $340,000 tax-free. The same contribution made in 2031 — just five years later — becomes approximately $210,000. The $130,000 difference is the exact cost of analysis paralysis.

Where can I open a free investment account in 2026?

The most beginner-friendly platforms in 2026 with $0 commissions and no account minimums:

- Fidelity — zero expense ratio index funds (FZROX, FZILX), fractional shares, Roth IRA; best overall for beginners

- Vanguard — inventor of low-cost index investing; best for long-term buy-and-hold investors

- Schwab — excellent educational resources, zero commissions, fractional shares

- SoFi — highest J.D. Power 2026 DIY investor satisfaction score; ETFs from $5

- TreasuryDirect.gov — I Bonds and TIPS directly from the U.S. government; no fees, no intermediary

Sources: RetailInvestor.org — Beginner Investing Guide 2026 · Nasdaq — How to Build a Million-Dollar Roth IRA 2026 · StockEducation.com — Stocks for Beginners 2026 · Money.com — Best Roth IRAs 2026 · CNBC — Smartest Way to Max IRA 2026 · Origin — 10 Best Investments Beginners 2026 · WealthKeel — Roth IRA Kickstart 2026 · BLS CPI March 2026 · Federal Reserve FOMC April 29, 2026 · TreasuryDirect.gov — I Bond Rates 2026

© Fact and View, 2026. For informational purposes only. Not investment advice. Consult a qualified financial advisor before making investment decisions.

Be First to Comment