On May 12, 2026, the Federal Reserve Bank of New York published its Q1 2026 Household Debt and Credit Report. The headline: total household debt reached $18.8 trillion — approaching an all-time record. Buried in the detail was something more alarming: the share of Americans behind on credit cards, auto loans, and student loans simultaneously hit levels not seen since the 2008 financial crisis.

Credit card balances alone reached $1.252 trillion as of Q1 2026 — up $482 billion since Q1 2021, a 63% increase in five years. That is $325 billion higher than the previous pre-pandemic record set in Q4 2019. And the average APR on cards currently carrying a balance sits at 21.52% — the highest sustained level since the Federal Reserve began tracking it.

This is not a story about reckless spending. It is a story about what happens when three years of inflation collide with record-high interest rates, stagnant wage growth, and a housing market that has locked millions of Americans into renting while their costs compound. Credit card debt is the pressure valve of a household economy under structural strain. And in 2026, that valve is near its limit.

The Big Picture: $1.3 Trillion in Revolving Debt

The credit card debt explosion is the direct result of three forces operating simultaneously since 2022. Understanding each one is essential to understanding why the numbers look the way they do — and why they won’t automatically resolve when inflation eases.

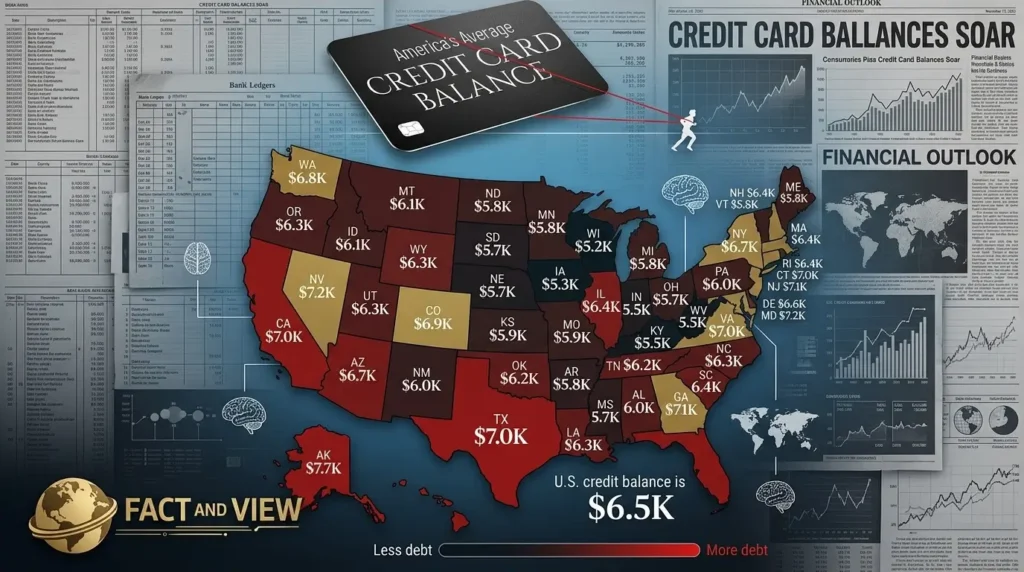

Fact: Total US credit card balances hit $1.252 trillion as of Q1 2026, according to the New York Fed’s Consumer Credit Panel. This follows a Q4 2025 peak of $1.277 trillion — the highest balance since the New York Fed began tracking this data in 1999. Credit card balances have risen by $482 billion since Q1 2021, a 63% increase in five years, and stand $325 billion above the pre-pandemic record of $927 billion in Q4 2019.

Fact: The May 12, 2026 FRBNY report showed the share of Americans behind on a range of household consumer debts reached all-time highs in Q1 2026 — with auto loan delinquency at the highest rate ever recorded, credit card delinquency near 2008 crisis levels, and student loan delinquency at its worst since before the COVID-era payment pause.

Fact: The average credit card APR sits above 21% — the highest sustained level since the Federal Reserve began tracking it. Inflation has pushed everyday costs up for three consecutive years, and millions of Americans have leaned on plastic just to cover basics like food, utilities, and medical bills. The debt load is growing faster than incomes in almost every income bracket below the top 20%.

The View: The $1.3 trillion credit card balance figure is the financial fingerprint of structural household stress. When credit card debt rises in boom years — as it did in 2018–2019 — it typically reflects discretionary spending and consumer confidence. When it rises as it has in 2022–2026, driven by food, utilities, housing costs, and medical bills, it reflects a survival mechanism. Americans are not spending their way into debt. They are inflating their way into it — and paying 21% annual interest for the privilege of keeping the lights on.

Related reading: Interest Rates Explained: How They Affect Your Money in 2026 — the full mechanics of how Fed rate decisions translate directly into the 21%+ APRs destroying household balance sheets.

Deep Dive: Six Structural Drivers of the Credit Card Debt Explosion

1. Inflation Built the Balance; Interest Compounded It

The credit card debt surge follows the exact trajectory of the consumer price surge that preceded it.

Fact: Credit card balances increased by more than $400 billion between Q1 2022 and Q4 2025 — one of the sharpest increases on record — in part due to rising prices for food, housing, utilities, and other essential expenses. The shift has turned toward supporting essential spending rather than discretionary purchases as before. By late 2025, total revolving credit exceeded $1.2 trillion, crossing the $1.3 trillion mark by early 2026.

The compound math is what makes this structurally dangerous. A household that charged $5,000 in essential expenses in 2022 — groceries, car repairs, medical bills — and made minimum payments has not paid off that balance in 2026. At 21% APR with minimum payments, a $5,000 balance takes approximately 15 years to pay off and costs $4,000+ in interest — nearly doubling the original debt. Inflation created the balance; interest is compounding it indefinitely.

2. APRs of 21%: The Highest Sustained Rate in History

The Federal Reserve’s 2022–2023 rate-hiking cycle raised the federal funds rate from near-zero to 5.5%. Credit card issuers repriced immediately — because credit card rates are explicitly tied to the prime rate and can be adjusted within a single billing cycle.

Fact: For all credit cards, the average APR in Q1 2026 was 21.00%. For cards accruing interest, the average was 21.52%. For new credit card offers, the average is 23.79%, per the Federal Reserve’s G.19 consumer credit report.

Fact: The Fed has held its benchmark rate at 3.5%–3.75% since December 2025, with zero cuts priced in for 2026. This means credit card APRs will remain above 20% for the entirety of 2026 at minimum. For the approximately 45% of adult credit cardholders who carry a balance at least one month per year, this is a permanent elevated cost — not a temporary peak.

The View: Credit card rates adjusting upward in 72 hours when the Fed raises rates is a feature of the financial system, not a bug. But the asymmetry is stark: when rates fall, issuers adjust downward slowly, citing “risk pricing” and “credit loss reserves.” The spread between the federal funds rate and the average credit card APR has widened since 2022 — issuers captured the rate increase fully and will return only a fraction of any future cut. This is a structural transfer of wealth from cardholders to financial institutions, institutionalized and normalized by the regulatory environment.

3. Delinquency Approaching 2008 Levels — With Different Demographics

The delinquency picture reveals that the debt explosion is not evenly distributed.

Fact: The 90-day-plus delinquency rate reached 3.2% in 2026 — a level not seen since the 2008–2009 financial crisis, per Moody’s Analytics and TransUnion Industry Insights Q1 2026.

Fact: Adults aged 18–29 are transitioning into 90-day credit card delinquency at roughly three times the rate of borrowers aged 60–69, according to New York Fed analysis. For Gen Z, shorter credit histories mean that late payments hit their credit scores disproportionately hard, raising future borrowing costs and making recovery slower. Nevada carries the nation’s highest credit card delinquency rate at 16.28% — where tourism-driven incomes, high living costs, and 22%+ APRs turn manageable balances into unmanageable spirals within months of missing a single payment.

The View: The demographic concentration of delinquency in younger borrowers is both a personal finance crisis and a macroeconomic warning signal. Young borrowers who accumulate delinquencies in their 20s face damaged credit scores that raise borrowing costs for the next 7 years — suppressing their ability to qualify for mortgages, auto loans, and business credit precisely during their prime wealth-building years. This creates a compounding disadvantage: inflation drove them into debt; high APRs trapped them; delinquency will follow them.

4. The “Normal” Trap: 49% of Americans Think Debt Is Fine

Perhaps the most consequential data point in the entire credit card debt story is not a balance figure. It is an attitude.

Fact: A Bankrate 2026 survey found that 53% of both Gen Xers and Millennials carry a credit card balance month to month — and 49% of Americans surveyed described credit card debt as “normal.” That normalization, more than any single statistic, may be the most consequential long-term finding.

When debt becomes culturally normalized, it stops triggering the behavioral responses that contain it. People stop comparing it to investing returns, stop calculating payoff timelines, stop treating the 21% APR as the emergency it mathematically is. The most dangerous thing about credit card debt in 2026 is not the $1.3 trillion balance — it is that nearly half of American adults have stopped being surprised by it.

5. The Macroeconomic Transmission: From Household Debt to Consumer Spending

Credit card delinquency doesn’t stay in a household’s balance sheet. It flows into the broader economy through three channels.

The consumer spending contraction: A household dedicating 20–25% of its disposable income to credit card minimum payments has dramatically less to spend on restaurants, retail, travel, and discretionary categories. With 45% of cardholders carrying balances, the aggregate demand drag from servicing $1.3 trillion in revolving debt at 21% is a measurable headwind to GDP growth.

The banking system stress: After hitting a series peak in Q1 2025 for large bank credit card data, the charge-off rate eased to 4.04% in Q2 2025 — but remains at levels dramatically elevated relative to pre-pandemic norms. Rising charge-offs reduce bank profitability, tighten future credit availability, and raise the credit standards that other household borrowers face.

The consumption inequality effect: High-income households pay off balances monthly and earn rewards. Lower-income households carry balances and pay 21%+ interest. Credit cards function as a redistribution mechanism in reverse — transferring wealth from lower-income borrowers to higher-income shareholders of financial institutions.

6. The OBBBA Credit Card Cap: Policy Response That Hasn’t Arrived

The White House proposed capping credit card interest rates at 10% as part of its affordability agenda — a campaign promise aimed directly at the households hit hardest by 21%+ APRs. As of May 2026, that cap is not law.

Fact: The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, did not include a credit card interest rate cap. Legislative negotiations stripped it from the final bill. The provision remains a policy proposal, not an enacted protection. Individual cardholders in 2026 have no regulatory protection from 21%+ APRs under current federal law.

The View: The credit card rate cap debate illustrates the structural tension in consumer finance regulation. Issuers argue that rate caps reduce credit availability for subprime borrowers. Consumer advocates argue that 21%+ rates are predatory regardless of availability. Both arguments have merit — but neither resolves the immediate problem for the 45% of American cardholders carrying a balance into 2026 at 21.52% APR. Waiting for legislative relief is not a financial strategy.

Related reading: New US Laws in 2026: What They Mean for Americans — the OBBBA provisions that did and did not pass, including the credit card rate cap that was proposed but not enacted.

Risks & Opportunities: Three Scenarios

Base Case (~50% probability): Debt Plateaus, Delinquency Stabilizes

The Q1 2026 balance decline to $1.252 trillion continues modestly through mid-year as seasonal paydowns occur. The Fed holds rates. APRs stay above 20%. Delinquency stabilizes near current elevated levels but doesn’t spike further. Household spending contracts modestly on debt service.

What this means for you: No relief from APRs in 2026. Every dollar of credit card balance you carry costs you 21 cents in interest per year — guaranteed. Paying it down is the highest-certainty financial return available to any American consumer.

Upside Scenario (~25% probability): Fed Cuts, APRs Ease in 2027

Iran diplomatic resolution reduces energy prices. Inflation falls to 2.5% by Q3. The Fed delivers two cuts. Credit card APRs fall toward 18%–19% in 2027 — still high, but meaningfully lower. Household debt service burden eases.

What this means for you: Some relief arrives — but 18% is still 18%. The only real solution is balance elimination. A one-percentage-point APR reduction saves approximately $100/year on a $10,000 balance. That’s meaningful but not transformative.

Downside Scenario (~30% probability): Delinquency Spikes, Credit Standards Tighten

Middle East conflict escalates. Inflation returns above 4%. Unemployment rises. Delinquency rates break through 4% on 90-day-plus — approaching 2009 peaks. Banks tighten credit standards. Households cut off from revolving credit face liquidity crises. Consumer spending contracts sharply.

What this means for you: This is the scenario where household financial resilience matters most. Emergency funds of 3–6 months of expenses become critical buffers. Households without savings are forced to deepen debt or default. Credit score damage at this scale takes 7+ years to repair.

Related reading: What Happens If US Debt Keeps Rising? — the fiscal context that is keeping the Fed frozen and APRs elevated simultaneously.

The Bottom Line

Credit card debt exploding in America in 2026 is not a story about individual financial irresponsibility. It is a story about three years of above-target inflation forcing households to use revolving credit for essentials — in an environment where that credit costs 21% annually and the political will to cap those rates has not materialized.

Your four-step action plan — right now:

1. Calculate your exact debt service cost. List every card balance, its APR, and the minimum payment. Total the annual interest you are paying. For most households carrying the average $6,580 individual balance at 21.52%, that is approximately $1,416 in annual interest going to zero productive use.

2. Avalanche method, starting today. List balances from highest APR to lowest. Pay minimums on all; direct every additional dollar to the highest-APR card. This mathematically minimizes total interest paid and eliminates balances fastest. Use Bankrate’s debt payoff calculator to model your exact timeline.

3. Stop using the cards you’re paying down. Using a card while trying to pay it off is the financial equivalent of bailing water with a colander. Freeze — literally if necessary — the cards you are eliminating and use a debit card for current spending.

4. Build $1,000 in emergency savings before anything else. The most common driver of new credit card debt is an unexpected expense — a car repair, a medical co-pay, a utility spike. A $1,000 cash emergency fund in a high-yield savings account (currently paying 4.5%–5%) absorbs most financial surprises without requiring new revolving debt.

The 21% APR environment will not be fixed by the Fed in 2026. It will not be capped by Congress in 2026. The only variable in the credit card debt equation that you fully control is your balance.

Every dollar of high-interest revolving debt you eliminate delivers a guaranteed 21% risk-free return. No investment in 2026 — not gold, not Nvidia, not private credit — offers that combination of guaranteed return and zero risk.

FAQ

How much credit card debt do Americans have in 2026?

Americans’ total credit card balance is $1.252 trillion as of Q1 2026, according to the New York Fed’s Consumer Credit Panel — down slightly from the Q4 2025 peak of $1.277 trillion, the highest balance since the New York Fed began tracking this data in 1999. Credit card balances have risen by $482 billion since Q1 2021, a 63% increase in five years, and stand $325 billion above the pre-pandemic record set in Q4 2019. The average individual credit card debt hit $6,580 per person in 2026, per ElitePersonalFinance’s analysis. Track current official data at the New York Fed’s Household Debt and Credit Report.

What is the average credit card interest rate in 2026?

For all credit cards, the average APR in Q1 2026 was 21.00%. For cards accruing interest, the average was 21.52%. For new credit card offers, the average is 23.79%, per the Federal Reserve’s G.19 consumer credit report. These are the highest sustained APR levels since the Federal Reserve began tracking credit card rates. At 21.52%, a $10,000 balance costs approximately $2,152 in annual interest if only minimum payments are made. Monitor current APR data at Bankrate’s credit card APR index and the Federal Reserve G.19 Release.

Why are credit card interest rates so high in 2026?

Credit card rates are directly tied to the federal funds rate — specifically the prime rate, which equals the federal funds rate plus 3 percentage points. When the Fed raised its benchmark from near-zero in 2022 to 5.5% by 2023, credit card issuers immediately repriced APRs upward. The Fed has held at 3.5%–3.75% since December 2025, with zero cuts priced in for 2026 — meaning APRs will stay above 20% through year-end. The additional factor: credit card issuers have widened their spread above the prime rate during the cycle, capturing the full rate increase while returning only a fraction of any eventual cut.

How bad is US credit card delinquency in 2026?

As of Q1 2026, the Federal Reserve Bank of New York reported that the share of Americans behind on household consumer debts reached all-time highs — with auto loan delinquency at the highest rate ever recorded and credit card delinquency near levels last seen at the height of the 2008 financial crisis. The 90-day-plus delinquency rate reached 3.2% in 2026, per Moody’s Analytics and TransUnion Industry Insights. Adults aged 18–29 are transitioning into 90-day delinquency at three times the rate of borrowers aged 60–69, with Nevada carrying the nation’s highest state delinquency rate at 16.28%.

Is the OBBBA credit card rate cap going to lower my APR?

No — not in its current form. The White House proposed a 10% credit card interest rate cap as part of its affordability agenda, but this provision was stripped from the final One Big Beautiful Bill Act signed July 4, 2025. No federal credit card rate cap exists as of May 2026. Individual cardholders have no statutory protection from rates of 21%+. Legislative action on this issue is pending but not scheduled for a vote in 2026.

What’s the fastest way to pay off credit card debt?

The avalanche method — paying minimums on all cards and directing extra payments to the highest-APR card first — minimizes total interest paid and eliminates debt fastest on a mathematical basis. The snowball method (lowest balance first) is slower mathematically but provides psychological wins that improve completion rates for some borrowers. Both are superior to minimum payments only, which at 21.52% APR can turn a $5,000 balance into a 15-year, $9,000 total payoff. Use Bankrate’s debt payoff calculator to model your specific timeline under both methods.

Where can I track US credit card debt and delinquency data in real time?

Primary sources, all free and authoritative:

- NY Fed Household Debt and Credit Report — quarterly official credit card balance and delinquency data

- Federal Reserve G.19 Consumer Credit Release — monthly APR data for all consumer credit products

- LendingTree Credit Card Statistics 2026 — quarterly aggregated analysis of Fed and NY Fed data

- Bankrate APR Index — weekly average credit card rates from the 50 largest US issuers

- CFPB Consumer Credit Card Market Report — annual deep-dive on credit card industry practices and consumer outcomes

- TradingEconomics — US Credit Card Delinquency Rate — historical delinquency rate with Fed data sourcing

Sources: Federal Reserve Bank of New York — Q1 2026 Household Debt and Credit Report, May 12, 2026 · Protect Borrowers — Record Financial Distress, May 12, 2026 · LendingTree — 2026 Credit Card Debt Statistics · ElitePersonalFinance / Yahoo Finance — Average Credit Card Debt Hits Record $6,580, March 17, 2026 · The Global Statistics — Credit Card Debt Statistics US 2026 · The Global Statistics — US Credit Card Debt Statistics 2026, April 15, 2026 · TradingEconomics — US Credit Card Delinquency Rate · Federal Reserve G.19 Consumer Credit Release, Q1 2026

© Fact and View, 2026. For informational purposes only. Not financial advice.

Be First to Comment