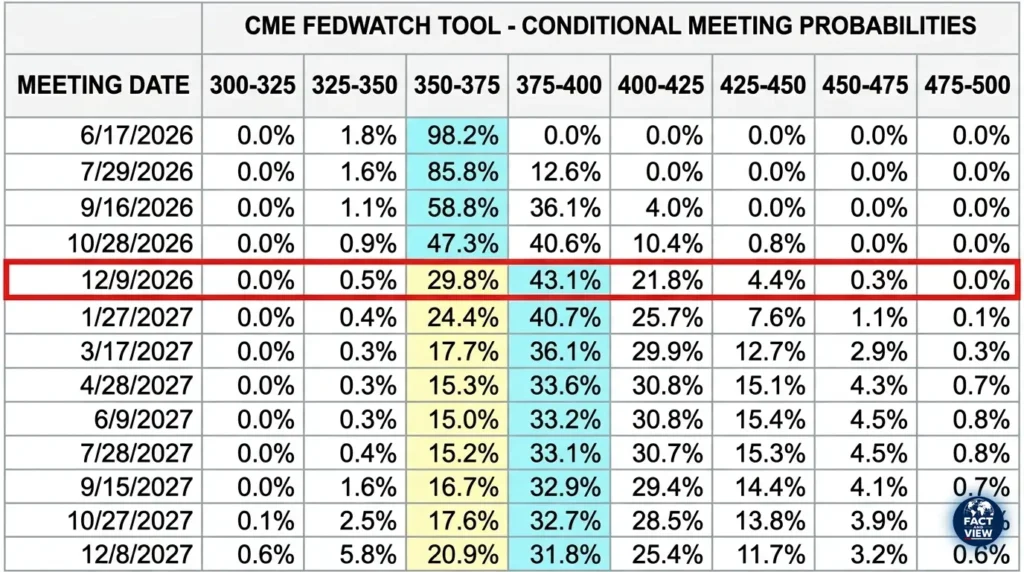

President Trump nominated Kevin Warsh to lead the Federal Reserve specifically because Warsh had spent the prior year publicly favoring lower interest rates. On June 17, 2026 — Warsh’s first meeting as chairman — the Fed held rates steady and signaled that its next move could be an increase, not a cut.

The Fed’s rate-setting committee released updated quarterly projections showing nine of nineteen policymakers now support higher rates in 2026, with six of those nine backing two separate quarter-point increases. Three months earlier, in March, not a single policymaker had penciled in a hike for the year — the committee’s consensus pointed toward one cut. The reversal is almost total, and it happened in a single quarter.

The proximate cause is inflation. The April 2026 Consumer Price Index showed headline inflation at its highest level in more than three years. Fed officials now project the personal consumption expenditures index will run at 3.6% by year-end — up from a 2.7% projection just three months ago. The question dividing Washington is whether tightening monetary policy now is the necessary medicine for an inflation problem that has lingered for five straight years, or whether it risks choking off growth in an economy already showing signs of labor market softening.

The View from the Right: Inflation Discipline, With a Side of Frustration

The conservative position on Fed policy in 2026 is more internally divided than at any point in recent memory — because the president’s own monetary policy preferences are now in direct tension with the chairman he selected.

On Trump’s stated position: The president has repeatedly asserted that lower interest rates will lead to higher economic output and “growth without inflation,” and that there is no meaningful inflation trade-off from easier monetary policy. Trump nominated Warsh explicitly because Warsh had signaled support for rate cuts — Pantheon Macroeconomics’ Samuel Tombs wrote at the time of nomination that “it’s reasonable to assume that he told the President he favors reducing interest rates today, otherwise he would not have been nominated.”

On Warsh’s actual framework: Once installed, Warsh has offered a more nuanced supply-side justification than a simple political accommodation. He has called artificial intelligence “the most productivity-enhancing wave of our lifetimes — past, present and future,” arguing that AI-driven output gains will eventually allow the Fed to cut rates aggressively without reigniting inflation. As of May 2026, independent economic data does not yet contain evidence of this supply-side expansion materializing at the scale Warsh’s framework requires — a gap that has not stopped him from articulating the theory as his long-term policy rationale.

On institutional independence: Despite the policy disagreement, Trump has notably softened his public pressure campaign. He told the Washington Examiner in recent weeks that he would “allow Warsh to do what he wanted to do” — a marked change from his treatment of former chair Jerome Powell, whom he repeatedly called “an American disgrace” over rate decisions and whose Fed faced a Trump administration criminal investigation that Powell himself described as a “pretext” to force rate cuts.

On the inflation-fighting case: Fed Governor perspectives within the institution split sharply. Several FOMC participants in January 2026 indicated further rate reductions would be appropriate if inflation continued declining as expected — but others argued for holding steady, and some explicitly raised the possibility that increases could become necessary if inflation remained persistently above target. By June, the latter camp had grown to a majority.

The View from the Left: A Self-Inflicted Wound Hitting Working Families

Progressive and Democratic-aligned economists frame the current inflation surge — and the resulting rate-hike signal — as a consequence of the administration’s own trade and fiscal policy choices, not an externally imposed shock the Fed must heroically resist.

On the inflation drivers: Equitable Growth’s May 2026 analysis is explicit: contrary to President Trump’s inflation optimism, the most recent reports show inflation running well above the Fed’s 2% target, with no evidence yet of the offsetting supply-side expansion that would justify the administration’s growth-without-inflation framing. The Iran war’s energy price shock, the OBBBA’s deficit-financed tax cuts, and the cumulative tariff pass-through to consumer goods are all cited as inflation sources independent of any Fed policy choice.

On labor market risk: Federal Reserve Governor Stephen Miran — appointed during the Trump administration but publicly dissenting from the emerging hawkish consensus — warned in a Dallas Fed speech that “the biggest risk… is that we’re misconstruing just how tight monetary policy is.” Miran argued current rates are tighter than necessary even accounting for supportive fiscal measures like the OBBBA’s tax cuts, and said he has “a hard time being concerned about inflation,” noting very low shelter inflation could offset price pressures elsewhere in the basket.

On political accountability: Critics note the asymmetry in how the administration discusses Fed independence. Trump spent over a year publicly attacking Powell for not cutting rates aggressively enough, including personal insults and an investigation Powell called politically motivated — yet has shown immediate deference to Warsh’s data-driven decision to hold rates and signal hikes, accepting “that Warsh will this week announce that the Fed is holding interest rates steady, just as Powell has done since December,” without the public criticism that defined the Powell era. Progressive commentators frame this as confirmation that the independence attacks were about loyalty, not policy substance.

On distributional impact: The labor market backdrop matters for how the Left frames the human cost of continued tightening. Fed officials’ own June 2026 projections hold unemployment steady at 4.3% for 2026 — but progressive economists note that “steady” unemployment masks deteriorating job-finding rates for new entrants and stagnant real wage growth for workers whose cost of living has risen faster than their paychecks throughout the inflationary period.

Economic and Household Dimensions: What the Numbers Show

The inflation trajectory that triggered the reversal:

| Period | Fed PCE Inflation Projection | Policy Stance |

|---|---|---|

| December 2025 | 2.4% (2026 forecast) | One cut expected in 2026 |

| March 2026 | 2.7% (2026 forecast) | One cut still expected, GDP raised to 2.4% |

| June 2026 | 3.6% (2026 forecast) | Nine of 19 officials favor hikes; six back two hikes |

The committee vote shift:

- March 2026: Zero policymakers favored a hike for the year; committee consensus was one rate cut

- June 2026: Nine of nineteen policymakers favor higher rates this year; six of those nine specifically back two quarter-point increases

What a hike means for household borrowing costs:

The federal funds rate has held at 3.5%–3.75% since the Fed’s last cut in December 2025. A single 25-basis-point hike would push the range to 3.75%–4.00%; two hikes would reach 4.00%–4.25%. Based on historical pass-through patterns:

- 30-year mortgage rates, currently near 6.5%, would likely rise toward 6.75%–7.0% under a two-hike scenario, adding approximately $70–$140/month to payments on a $400,000 loan

- Credit card APRs, already averaging above 21%, would climb further, since card rates are explicitly indexed to the prime rate (federal funds rate plus 3 percentage points)

- Auto loan rates, currently near 7% for new vehicles, would extend the affordability squeeze already pushing average monthly payments toward $773

The CPI reality consumers are experiencing right now:

April 2026 CPI showed headline inflation at its highest level in over three years. March 2026 PCE inflation registered 3.5% year-over-year — both measures moving in the wrong direction relative to the Fed’s 2% target, and both substantially above the administration’s stated optimism about disinflation.

The labor market backdrop:

Fed officials project unemployment will hold at 4.3% through 2026 and 2027 — broadly stable, which is precisely why hawkish committee members feel they have room to prioritize inflation without an immediate growth-policy trade-off. The GDP growth projection for 2026 stands at 2.2%, a modest downgrade from March’s 2.4% forecast — the first tangible sign that tighter-for-longer policy expectations are beginning to shave growth estimates.

Conclusion: A Hawkish Pivot With an Open Outcome

The Federal Reserve under Kevin Warsh enters the second half of 2026 in a position that confounds the simple political narrative that accompanied his nomination. He was selected as the rate-cutter the president wanted. His first meeting produced a signal toward rate increases — a decision driven by inflation data that both parties’ own economists acknowledge is genuinely elevated, regardless of which policy choices contributed to it.

What the data confirms with bipartisan agreement:

- April 2026 CPI inflation reached its highest level in more than three years

- The Fed’s own committee shifted from zero members favoring a hike in March to nine of nineteen favoring hikes in June

- Fed officials raised their year-end PCE inflation projection from 2.7% to 3.6% in a single quarter

- Unemployment is projected to remain stable at 4.3% through 2026–2027, removing the most common justification for immediate rate cuts

What remains genuinely contested:

- Whether the inflation surge is primarily attributable to the Iran war energy shock, tariff pass-through, OBBBA fiscal stimulus, or some combination — a question with direct implications for whether monetary tightening is the correct tool to address it

- Whether Warsh’s AI-productivity thesis will materialize quickly enough to justify the rate cuts he was nominated to deliver, or whether — as Equitable Growth’s analysis suggests — the supply-side evidence simply isn’t there yet

- Whether Governor Miran’s minority view, that current policy is already tighter than the data justifies, gains traction as 2026 progresses, or whether the hawkish majority’s two-hike scenario actually materializes

For American households, the practical stakes are immediate regardless of which political framing proves correct. A Fed that hikes rates twice in 2026 means mortgage, auto, and credit card costs that were already elevated climb further before any relief arrives — a direct continuation, not a reversal, of the borrowing-cost environment defined throughout the Powell era and now extended under different leadership with a different stated mandate.

Continue reading from Fact and View:

- What the Federal Reserve Really Does (Simple Explanation) — the full mechanics of how Fed decisions become mortgage rates, credit card APRs, and savings yields

- Interest Rates Explained: How They Affect Your Money in 2026 — the six borrowing categories most exposed to a hike scenario

- Middle East Tensions Explained: What It Means for Oil Prices — the energy shock that NPR and Fed officials directly cite as the catalyst pushing rate cuts off the table

FAQ

Did the Federal Reserve raise interest rates in June 2026?

No — the Fed held its benchmark rate steady at 3.5%–3.75% at its June 17, 2026 meeting, the first under new Chairman Kevin Warsh. However, the committee’s updated quarterly projections showed nine of nineteen policymakers now support raising rates later in 2026, with six of those nine backing two separate quarter-point increases — a sharp reversal from March 2026, when no committee members favored a hike and the group’s consensus pointed toward a rate cut.

Why did the Fed signal possible rate hikes instead of the cuts Trump wanted?

Inflation data deteriorated sharply between March and June 2026. The Fed’s year-end PCE inflation projection rose from 2.7% to 3.6% in a single quarter, and April 2026 CPI showed headline inflation at its highest level in more than three years. A wartime spike in energy prices tied to the Iran conflict is widely cited as a key driver. With unemployment projected to remain stable at 4.3%, the committee’s hawkish majority concluded there was room to prioritize inflation control without an immediate trade-off against employment — overriding the rate-cut preference that motivated Trump’s selection of Warsh in the first place.

Who is Kevin Warsh and why does his appointment matter?

Kevin Warsh is a former Federal Reserve governor (2006–2011) who succeeded Jerome Powell as Fed chair in May 2026. Trump nominated him after Warsh publicly signaled support for lower interest rates — a reversal from Warsh’s earlier career as an inflation hawk during the 2008 financial crisis. Warsh has vowed the Fed will remain “strictly independent,” and his first policy decision — holding rates with a hawkish signal — has already demonstrated a willingness to diverge from the rate-cut outcome his nomination was expected to deliver. He has also proposed a supply-side justification for eventual cuts, arguing AI-driven productivity gains could allow rate reductions without reigniting inflation.

How would a Fed rate hike affect my mortgage and credit card payments?

If the Fed delivers the two quarter-point hikes that six of nineteen committee members currently favor, the federal funds rate would rise from 3.5%–3.75% to approximately 4.00%–4.25%. Based on historical pass-through, 30-year mortgage rates — currently near 6.5% — could rise toward 6.75%–7.0%, adding roughly $70–$140 per month to payments on a $400,000 loan. Credit card APRs, already averaging above 21% and directly indexed to the federal funds rate plus a fixed margin, would climb further. Auto loan rates, currently near 7% for new vehicles, would extend the affordability pressure already pushing average monthly payments toward $773.

What is Governor Stephen Miran’s dissenting view on Fed policy?

Federal Reserve Governor Stephen Miran has publicly argued that current monetary policy is tighter than necessary, warning in a Dallas Fed speech that “the biggest risk… is that we’re misconstruing just how tight monetary policy is.” Miran contends that very low shelter inflation could offset price pressures elsewhere in the consumer basket and that he has “a hard time being concerned about inflation” given that backdrop. His position represents the most prominent dovish dissent within the current Fed leadership, standing in contrast to the nine-of-nineteen hawkish majority that emerged in June 2026.

Where can I track Federal Reserve interest rate decisions and projections in real time?

Primary sources for monitoring Fed policy:

- Federal Reserve FOMC Calendar and Statements — official meeting dates, statements, and projections

- Federal Reserve Summary of Economic Projections — the quarterly “dot plot” showing individual policymaker rate expectations

- CME FedWatch Tool — live market-implied probability of future Fed rate moves

- BLS Consumer Price Index — official monthly inflation data

- TradingEconomics — US Interest Rate — historical and current rate tracking with policy news

Sources: CBS News — Kevin Warsh First FOMC Meeting, June 17, 2026 · PBS NewsHour — Warsh First Press Conference, June 17, 2026 · NPR — Fed Holds Rates, Hints at Hike, June 17, 2026 · CNBC — Trump Sworn In Warsh as Fed Chair, May 22, 2026 · Equitable Growth — Inflation, Interest Rates, and the New Fed Chair, May 18, 2026 · Washington Examiner — Warsh-Led Fed Holds Rates Steady, June 2026 · TradingEconomics — Fed Policy Timeline 2026 · AOL/CNN — Trump Nominates Warsh, May 2026

© Fact and View, 2026. This article presents documented perspectives from multiple sources. It does not represent an editorial endorsement of any monetary policy position.

Be First to Comment