A Privilege Under Pressure From an Unexpected Direction

For eighty years, the central threat to the U.S. dollar’s reserve currency status was assumed to come from rivals — the Soviet Union, then China, then a loosely organized bloc of sanctioned states seeking an alternative. In 2026, the most consequential pressure is coming from somewhere else entirely: America’s own allies.

Canadian Prime Minister Mark Carney announced a $25 billion sovereign wealth fund in early May 2026 explicitly designed to reduce Canada’s economic dependence on the United States. France completed the repatriation of all 129 tons of its gold held at the Federal Reserve Bank of New York between July 2025 and January 2026 — the first such withdrawal since the 1960s, when Paris feared U.S. debt would force a dollar devaluation. Both moves came from treaty allies, not adversaries.

Meanwhile, the dollar fell approximately 9% on a trade-weighted basis during Trump’s first year back in office — a decline that, unusually, reflects explicit U.S. policy goals as much as external market forces. The administration’s own economic architects have proposed deliberately weakening the dollar to fix America’s trade deficit, even as the Treasury Secretary insists publicly that a strong dollar remains the official policy. The reserve currency debate in 2026 is no longer simply about whether the dollar will lose its status. It is about whether the United States itself has decided that status is now more burden than benefit.

The View from the Right: A Divided House, Same Address

The conservative position on dollar policy in 2026 is not unified — it is split between two competing schools of thought operating inside the same administration, a division more consequential than the traditional left-right divide on this issue.

The traditional strong-dollar wing: Treasury Secretary Scott Bessent has repeatedly affirmed, including in a January 2026 CNBC appearance, that “the U.S. always has a strong dollar policy,” while adding the qualifier that “a strong dollar policy means setting the right fundamentals.” This represents the institutional Republican and broader Washington consensus dating back decades: dollar dominance lowers borrowing costs, reduces import prices for consumers, and gives the United States unmatched leverage through sanctions.

The “weak dollar school”: Council of Economic Advisers Chair Stephen Miran — now also a voting Federal Reserve governor — has proposed what’s been termed the “Mar-a-Lago Accord,” a strategy to deliberately weaken the dollar to reduce the U.S. current-account deficit and revive domestic manufacturing. Miran’s framework argues the dollar’s reserve status has become an economic burden, systematically overvaluing the currency and pricing American exporters out of global markets. Senior Counselor for Trade and Manufacturing Peter Navarro represents an allied “Make in America” wing that prioritizes manufacturing revival even at the cost of currency strength.

On stablecoins as a parallel strategy: Trump signed an executive order in January 2026 encouraging dollar-backed stablecoins issued by private firms — a policy both camps support for different reasons. The strong-dollar wing, including Bessent and Fed Governor Christopher Waller, argues stablecoins reinforce dollar primacy by creating new demand for U.S. Treasuries, since approximately 99% of stablecoins in circulation are dollar-denominated. As much as 80% of dollar-backed stablecoin flow already occurs outside the United States — extending dollar usage into economies like Argentina, Brazil, and Nigeria, where it serves as a hedge against local currency instability.

On the BRICS threat specifically: Trump’s position has been the most aggressive of any administration on currency competition, threatening 100% tariffs on BRICS nations if they create a rival currency, declaring “you leave the dollar, you are not doing business with the United States.” This reflects a view, shared broadly across the conservative coalition despite the strong/weak-dollar split, that any organized move away from the dollar represents a direct geopolitical challenge requiring forceful response.

The View from the Left: Self-Inflicted Erosion Through Weaponization

Progressive and Democratic-aligned economists trace the dollar’s declining position not to external rivals successfully building alternatives, but to the cumulative effect of U.S. policy choices — sanctions, tariffs, and unpredictability — that have made dollar exposure a liability for America’s own partners.

On the weaponization critique: Critics across the political spectrum, but most consistently from foreign policy and economics scholars aligned with internationalist Democratic positions, argue the U.S. has “weaponized the dollar,” particularly through sanctions imposed without allied coordination. A November 2025 Cambridge University Press analysis by political scientist Dongan Tan posited that U.S. sanctions could create a bifurcated global economic system — the U.S. and its allies on one side, China and BRICS countries on the other.

On the “paradox” driving allies away: EBC Financial Group analyst Sana Ur Rehman’s May 2026 analysis identifies what she calls a structural paradox: “the United States cannot both weaponize the dollar system and maintain universal trust in it.” Critically, Ur Rehman emphasizes that the current wave of diversification — Canada’s sovereign wealth fund, France’s gold repatriation — comes from “allies and partners who have watched the United States weaponize the dollar-based financial system, and have quietly concluded they need to reduce their exposure to it.” She calls this “different from anything in the past 80 years of dollar dominance” precisely because it originates with friends, not foes.

On tariff policy undermining the very system it claims to protect: The Atlantic Council’s December 2025 analysis notes a direct contradiction in administration policy: tariffs reduce the dollars flowing abroad through trade, which in turn reduces the foreign demand for dollar assets that has historically sustained American borrowing capacity. Foreign investors sold $63 billion in U.S. equities between March and April 2025 alone, with the dollar index falling 8% that year — a pattern Democratic-aligned critics argue is the direct, predictable consequence of an “America First” approach applied to currency policy.

On Fed independence as a related vulnerability: Former Fed Chair Jerome Powell stated in January 2026 that a Department of Justice investigation into his congressional testimony was politically motivated — widely interpreted by Democratic lawmakers and progressive economists as an attempt to pressure the central bank into rate cuts that would serve the administration’s preferred weak-dollar strategy. Critics argue that perceived threats to Fed independence compound foreign concerns about dollar reliability, since the credibility of any reserve currency depends partly on confidence that its central bank operates free from short-term political direction.

Economic and Household Dimensions: What Actually Changes for Americans

The “exorbitant privilege” Americans currently enjoy:

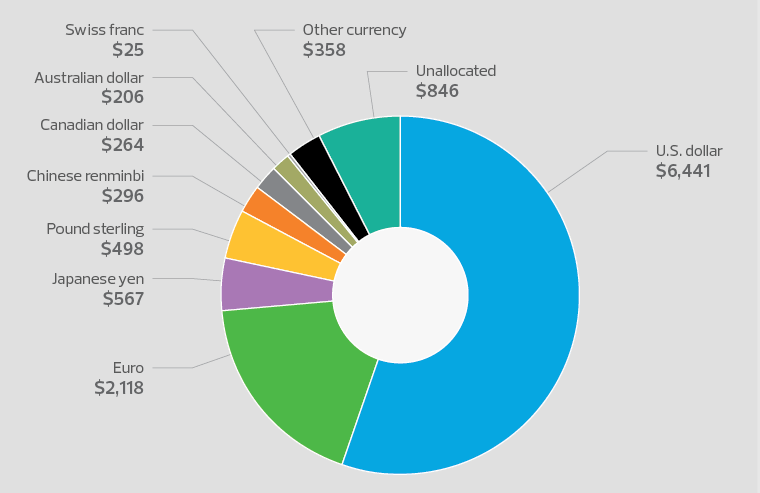

The dollar’s reserve status delivers concrete, measurable benefits that rarely appear on a household budget line but shape it indirectly. Dollar assets comprise approximately 59% of global foreign currency reserves, with the next largest currency, the euro, holding only about 20%. Roughly 64% of world debt is denominated in dollars. This dominance lowers U.S. government borrowing costs, reduces import prices by keeping the dollar’s purchasing power elevated, and insulates American consumers from the kind of currency crisis that periodically devastates countries reliant on foreign-currency borrowing.

What measurable erosion has occurred so far:

| Indicator | Change | Period |

|---|---|---|

| Dollar trade-weighted value | -9% | Trump’s first year back in office (2025–2026) |

| Dollar Index (DXY) | Fell to 95.5, lowest since 2022 | Early 2026 |

| Foreign equity sales | $63 billion sold | March–April 2025 |

| France’s gold repatriation | 129 tons moved from NY Fed to Paris | July 2025–January 2026 |

| IMF dollar reserve share | Declined to approximately 57–59% | From over 70% in 2001 |

The inflation and borrowing-cost tradeoff:

A weaker dollar is not uniformly bad or good for American households — it is a tradeoff with specific winners and losers. American exporters and domestic manufacturers benefit from a weaker dollar, since their goods become cheaper for foreign buyers. But a weaker dollar also makes imports more expensive — directly raising prices on every imported good, from electronics to clothing to auto parts, at a moment when CPI is already running at 3.3% and the Fed signaled in June 2026 that its next move could be a rate hike rather than a cut. NPR’s reporting on the internal Trump administration debate captured this tension directly: “a weakening dollar might be good for exporters, but it fuels inflation for consumers as imports get more expensive.”

The borrowing-cost connection to the national debt:

A weaker dollar combined with reduced foreign appetite for Treasuries directly threatens the financing of the $39 trillion national debt. The Committee for a Responsible Federal Budget projects debt could reach 134% of GDP by 2035 if current tariff and tax policies become permanent — a trajectory that becomes considerably harder to finance if foreign central banks continue reducing their dollar-denominated reserve holdings.

The stablecoin wildcard for ordinary consumers:

For younger Americans and anyone using cryptocurrency or international remittance services, the stablecoin dimension of dollar policy is increasingly tangible. Dollar-backed stablecoins are seeing significant adoption in countries like Argentina, Brazil, and Nigeria as a hedge against local currency instability — meaning U.S. dollar dominance is being extended through private financial technology even as official government-to-government reserve holdings diversify away from it.

Conclusion: Two Tracks Moving in Different Directions

The dollar’s reserve currency status in 2026 is not collapsing, and no credible analysis from either political perspective claims an imminent dethroning. The euro lacks a unified fiscal backer; the Chinese renminbi remains illiquid and subject to capital controls; the proposed BRICS “Unit” remains, by the admission of BRICS members themselves, more aspiration than functioning system. Indian Foreign Minister S. Jaishankar’s own assessment — “I don’t think there’s any policy on our part to replace the dollar… the dollar as the reserve currency is the source of global economic stability” — reflects the view of even nominally dollar-skeptical nations that no viable alternative currently exists.

What the data confirms with bipartisan agreement:

- The dollar fell approximately 9% on a trade-weighted basis during 2025–2026, partly as a result of deliberate U.S. policy choices

- Allied nations — not just geopolitical rivals — have taken concrete diversification steps, including Canada’s sovereign wealth fund and France’s gold repatriation

- The Trump administration itself is internally divided between a traditional strong-dollar Treasury position and a weak-dollar Mar-a-Lago Accord framework

- No current alternative — euro, renminbi, or BRICS currency — possesses the liquidity, trust, or network effects to replace the dollar in the near term

What remains genuinely contested:

- Whether deliberately weakening the dollar will succeed in reviving American manufacturing without triggering the inflation and reduced foreign Treasury demand that critics warn about

- Whether the erosion driven by allied diversification represents a permanent structural shift or a temporary reaction to a specific administration’s policies that could reverse under different leadership

- Whether stablecoin-driven dollar usage growth in emerging markets offsets official-sector reserve diversification, or whether the two trends are simply operating on different tracks entirely

For American households, the reserve currency question translates into a specific set of practical stakes: borrowing costs, import prices, and the government’s capacity to finance its debt without triggering a disruptive market response. Those stakes do not require the dollar to lose its reserve status to matter — the ongoing internal debate over how to manage that status, playing out between Bessent, Miran, and the broader international response to it, is already shaping the inflation and interest-rate environment every American is living through right now.

Continue reading from Fact and View:

- What Happens If US Debt Keeps Rising? — how dollar reserve erosion directly affects the financing of the $39 trillion national debt

- Fed Rate Hikes: Fighting Inflation or Slowing Growth? — the Fed independence questions intersecting with dollar policy debates

- Where Smart Money Is Moving Right Now (2026 Update) — the institutional gold-buying trend directly connected to dollar diversification

FAQ

Is the US dollar losing its reserve currency status in 2026?

Not imminently, but the trend is directionally negative. The dollar’s share of global foreign exchange reserves has declined to approximately 57–59%, per IMF data, down from over 70% in 2001. The dollar fell roughly 9% on a trade-weighted basis during 2025–2026, and allied nations including Canada and France have taken concrete diversification steps. However, most economists agree no current alternative — the euro, Chinese renminbi, or a proposed BRICS currency — has the liquidity, trust, and network effects needed to replace the dollar in the foreseeable future. The more accurate framing, per Brookings’ analysis, is a gradual shift toward a “multipolar” currency world rather than an imminent collapse of dollar dominance.

What is the Mar-a-Lago Accord and does the Trump administration actually want a weaker dollar?

The Mar-a-Lago Accord is a policy framework proposed by Stephen Miran, formerly chair of the Council of Economic Advisers and now a Federal Reserve governor, aimed at deliberately weakening the dollar to reduce the U.S. trade deficit and encourage manufacturing reshoring. The administration is internally divided: Treasury Secretary Scott Bessent maintains publicly that “the U.S. always has a strong dollar policy,” while Miran’s framework and allies like Peter Navarro favor currency weakening as a tool of trade policy. The dollar’s approximately 9% trade-weighted decline during 2025–2026 suggests the weak-dollar approach has had real effect regardless of the official rhetorical position.

Why are US allies like Canada and France reducing their reliance on the dollar?

Both moves are widely interpreted as responses to U.S. policy unpredictability rather than ideological opposition to the dollar itself. Canadian Prime Minister Mark Carney announced a $25 billion sovereign wealth fund in May 2026 explicitly aimed at reducing economic dependence on the United States. France completed repatriating all 129 tons of its gold held at the Federal Reserve Bank of New York between July 2025 and January 2026 — the first such move since the 1960s. Analysts including EBC Financial Group’s Sana Ur Rehman frame this as evidence that even close allies have concluded reduced dollar exposure is now prudent risk management, given the administration’s use of tariffs and sanctions as policy tools.

How does dollar weaponization through sanctions affect its reserve status?

Sanctions are widely cited as the single largest driver of de-dollarization sentiment globally. When the U.S. imposes sanctions — particularly without allied coordination — countries holding dollar reserves become aware they could be cut off from accessing those assets if targeted in the future. Russia’s central bank dollar holdings fell from $383 billion in January 2022 to roughly $130 billion by late 2023 following sanctions over Ukraine. China’s Cross-Border Interbank Payment System now processes an average of ¥9.6 trillion daily, used by more than 4,900 banking institutions across 187 jurisdictions, representing one infrastructure response to sanctions exposure concerns.

Could a BRICS currency realistically replace the US dollar?

Most experts assess this as unlikely in the near to medium term. The BRICS group has discussed a potential gold-backed currency called the “Unit,” but India’s Foreign Minister S. Jaishankar stated plainly in 2026 that “right now, there is no proposal to have a BRICS currency” and that BRICS members hold “very diverse positions” on the issue. Brazil, which held the BRICS rotating presidency in 2025, has said there are no plans for significant steps toward a common currency. The more realistic near-term development is expanded local-currency trade settlement and blockchain-based payment systems that reduce dollar dependency for specific transactions without creating a unified rival reserve currency.

How would losing reserve currency status affect ordinary Americans?

If the dollar’s reserve status meaningfully eroded, Americans would likely face higher borrowing costs (since foreign demand currently helps keep U.S. Treasury yields and, by extension, mortgage rates lower than they would otherwise be), higher import prices (since the dollar’s purchasing power would decline), and a reduced ability for the federal government to run large deficits without triggering inflation or a currency crisis. The Brookings Institution describes the current benefits as an “exorbitant privilege” — and notes that losing it would work in reverse, making the U.S. more susceptible to the kind of currency-driven economic shocks that countries with weaker reserve currencies regularly experience.

Where can I track dollar reserve currency trends and de-dollarization developments?

Primary sources for ongoing monitoring:

- IMF COFER Database — official quarterly data on the currency composition of global foreign exchange reserves

- Federal Reserve — Dollar Index Data — official U.S. dollar trade-weighted index

- Brookings — The Changing Role of the US Dollar — ongoing independent academic analysis

- Council on Foreign Relations — Mar-a-Lago Accord Tracker — policy implementation tracking

- World Gold Council — central bank gold purchase and reserve diversification data

Sources: Council on Foreign Relations — Mar-a-Lago Accord Ripple Effect, January 27, 2026 · NPR — Trump Weaker Dollar Debate, January 30, 2026 · Fortune — De-Dollarization Paradox, May 6, 2026 · Atlantic Council — Trump Administration Dollar Strategy, December 23, 2025 · Brookings — The Changing Role of the US Dollar · U.S. News — De-Dollarization 2026, April 2, 2026 · Investing News Network — BRICS Currency, February 24, 2026 · deVere Group — US Dollar Outlook 2026, April 20, 2026 · NPR Planet Money — Trump’s Tariff Advisors Transcript, April 24, 2025 · Aberdeen Investments — Mar-a-Lago Accord Analysis

© Fact and View, 2026. This article presents documented perspectives from multiple sources. It does not represent an editorial endorsement of any monetary or currency policy position.

Be First to Comment