When the Federal Reserve wants to cool down a too-hot economy, it has two main tools. The first — raising interest rates — gets most of the attention. The second is quieter, less visible, and arguably just as powerful: quantitative tightening.

If you’ve seen the phrase “QT” in financial news and wondered what it means, you’re not alone. Quantitative tightening is one of those monetary policy concepts that economists discuss constantly but rarely explain to ordinary people. That’s a problem, because QT affects your mortgage rate, your retirement account, and the government’s borrowing costs — whether you’re aware of it or not.

This guide explains quantitative tightening in plain English: what it is, how it works, why the Federal Reserve uses it, and what it actually means for your finances.

What Is Quantitative Tightening?

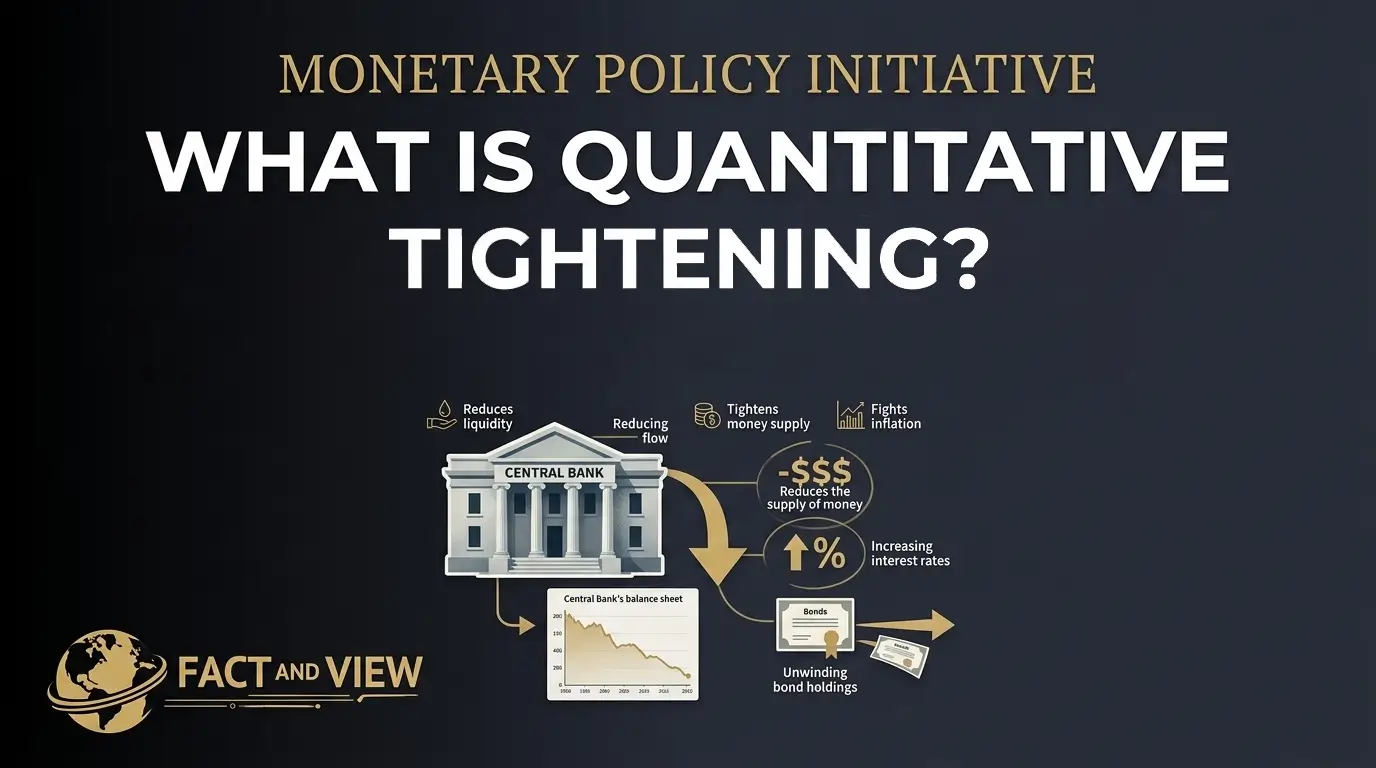

Quantitative tightening — or QT — is a process where the Federal Reserve shrinks the size of its balance sheet by allowing bonds it previously purchased to roll off without replacing them.

That sentence probably needs a little unpacking. Let’s start at the beginning.

The Federal Reserve’s balance sheet is essentially a record of everything the Fed owns. During economic crises — most notably during the 2008 financial collapse and the 2020 COVID-19 pandemic — the Fed purchased enormous quantities of U.S. Treasury bonds and mortgage-backed securities from banks. It paid for these purchases by creating new money electronically. This process is called quantitative easing (QE) — the opposite of quantitative tightening.

The goal of QE was to inject money into the financial system, push interest rates down, encourage borrowing and spending, and prevent the economy from collapsing. It worked, in the sense that economic activity continued. But it left the Fed holding a massive portfolio of assets — and the financial system flooded with money.

Quantitative tightening reverses this process.

Instead of buying more bonds, the Fed simply stops reinvesting when the bonds it holds mature. When a bond matures, the borrower (the U.S. Treasury, in most cases) repays the principal. Normally, the Fed would take that money and immediately buy a new bond to keep its holdings constant. During QT, it doesn’t. It lets the money disappear back out of the financial system.

The result: the money supply gradually contracts, the Fed’s balance sheet shrinks, and financial conditions tighten — which is precisely the goal.

How Quantitative Tightening Works, Step by Step

Step 1: The Fed owns bonds it bought during QE. At the peak of its balance sheet in 2022, the Federal Reserve held approximately $9 trillion in Treasury bonds and mortgage-backed securities — more than nine times what it held before the 2008 financial crisis.

Step 2: Some of those bonds reach maturity. Bonds have expiration dates, called maturity dates. When a Treasury note matures, the government repays the face value. The Fed receives that payment.

Step 3: During QE, the Fed reinvests. During QT, it doesn’t. In quantitative easing, the Fed takes that repayment and immediately buys a new bond — keeping its total holdings constant. In quantitative tightening, it lets the money sit, effectively removing it from the financial system.

Step 4: The money supply shrinks. Less money in the financial system means banks have less available to lend. Credit becomes scarcer. Interest rates tend to rise, or at least don’t fall as fast as they otherwise might. Asset prices may come under pressure.

Step 5: Financial conditions tighten. This is the intended effect. A tighter financial system reduces the kind of excessive borrowing, speculative investment, and inflationary pressure that QE helped create.

Related reading: What the Federal Reserve Really Does (Simple Explanation) — the full mechanics of how the Fed uses both interest rates and its balance sheet to manage the economy.

How Big Is the Fed’s Balance Sheet Right Now?

After peaking at nearly $9 trillion in April 2022, the Fed began its current quantitative tightening program in June 2022. Since then, the balance sheet has contracted by roughly $2 trillion, bringing it to approximately $6.7–$7 trillion by mid-2026 — still historically enormous, but meaningfully reduced.

The Fed has varied the pace of QT over time, sometimes allowing up to $95 billion per month to roll off the balance sheet, sometimes throttling back to $60 billion per month when market conditions looked fragile. Under new Fed Chair Kevin Warsh — who took office in May 2026 — QT has continued, though its long-term pace and endpoint remain subjects of active debate among economists.

Why Does Quantitative Tightening Matter to Ordinary Americans?

QT operates largely in the background — you can’t see it directly — but its effects travel quickly into everyday financial life.

Your mortgage rate. One of QT’s most direct household effects runs through the mortgage market. When the Fed stops reinvesting in mortgage-backed securities during QT, the supply of money available for new mortgages declines. That scarcity pushes mortgage rates higher. Analysts estimate QT may add anywhere from 0.25 to 0.50 percentage points to long-term interest rates compared to a world without it, contributing to the elevated 6.5% mortgage rates American homebuyers face in 2026.

Your savings and investment returns. QT drains excess liquidity from the banking system, which tends to push short-term interest rates up (or prevent them from falling). This is part of the reason high-yield savings accounts have paid 4–5% in 2026, compared to near-zero in 2021 when QE was pumping money into the system.

Your retirement account. A balance sheet that’s shrinking means less money flowing into financial markets — and some of that money had been helping support equity prices during the post-pandemic bull market. QT is one of the reasons the stock market has been more volatile and more sensitive to economic data in 2024–2026 than in the 2020–2021 period.

The national debt’s cost. When the Fed holds fewer Treasury bonds, the government must attract more private buyers to fund its deficit spending. Private buyers demand higher interest rates, which is one structural reason Treasury yields have remained elevated — adding billions to the government’s annual interest bill, which already exceeds $1 trillion per year.

Related reading: Interest Rates Explained: How They Affect Your Money in 2026 — the six borrowing categories most affected by the tight financial conditions QT helps sustain.

Benefits of Quantitative Tightening

It helps fight inflation. The most fundamental goal of QT is to reduce excess money in the financial system. Less money chasing the same goods means less upward price pressure — a direct contribution to bringing inflation back toward the Fed’s 2% target.

It rebuilds the Fed’s policy flexibility. A bloated balance sheet limits the Fed’s options. A normalized, smaller balance sheet gives the central bank more room to conduct future rounds of quantitative easing if the economy faces another crisis.

It reduces moral hazard. When the Fed perpetually buys assets, investors can fall into the habit of assuming the central bank will always step in to support markets — sometimes called the “Fed put.” QT signals that this backstop has real limits, encouraging more disciplined risk-taking in financial markets.

It improves savers’ returns. By tightening financial conditions and keeping interest rates higher than they would otherwise be, QT has directly benefited Americans with savings, CDs, money market funds, and short-duration bonds — groups that were punished by near-zero rates during the QE era.

Risks and Criticisms

QT can be destabilizing if it moves too fast. In September 2022, the Bank of England was forced to temporarily halt its quantitative tightening program when rapid balance sheet contraction contributed to a crisis in UK pension funds. In the U.S., rapid QT in 2023 contributed to stress in regional bank funding markets, prompting the Fed to create emergency lending facilities.

The “right” balance sheet size is unknown. Economists genuinely disagree about how small the Fed’s balance sheet can safely become before the banking system starts experiencing funding shortages. The Fed itself has said it will watch for signs of reserve scarcity and slow or stop QT accordingly.

QT works more slowly and less predictably than rate hikes. Rate changes take effect quickly and have well-studied economic transmission channels. QT’s effects are harder to measure and depend heavily on who is buying the bonds the Fed stops reinvesting in and at what yields.

It can conflict with other policy goals. In 2026, the Fed faces a situation where it is simultaneously considering rate hikes to fight inflation while QT continues to tighten financial conditions. Critics argue that running both tools simultaneously creates compounding tightening pressure that risks overshooting into an unnecessary recession.

Related reading: Fed Rate Hikes: Fighting Inflation or Slowing Growth? — how QT and rate hikes are currently operating together, and what that means for the economy in 2026.

Common Misunderstandings About Quantitative Tightening

Myth: Quantitative tightening means the Fed is selling its bonds. Reality: The Fed rarely sells bonds during QT. Instead, it simply stops reinvesting when bonds mature — a passive process called “roll-off.” Outright sales would be faster and more disruptive, which is why the Fed generally avoids them unless conditions are unusually strong.

Myth: QT and rate hikes are the same thing. Reality: They’re distinct tools that often work in the same direction but operate through different channels. Rate hikes directly set the short-term borrowing cost between banks. QT drains reserves from the banking system over time. Both tighten financial conditions, but through different transmission paths and with different timing.

Myth: Quantitative tightening means the Fed is “printing money in reverse.” Reality: This is partially accurate but overly simplified. During QE, the Fed created electronic reserves to buy bonds. During QT, those reserves disappear as bonds mature and are not replaced. But it’s not as simple as running a money printer backward — the effects on the broader economy and financial markets are more gradual and complex.

Myth: QT will definitely cause a recession. Reality: This is genuinely uncertain, and economists disagree. The U.S. economy weathered the 2022–2024 QT period without a technical recession, despite widespread predictions of one. Whether the current pace of balance sheet reduction will eventually tip the economy into contraction depends on how quickly the Fed adjusts and how resilient underlying demand remains.

Myth: QT only affects investors and doesn’t touch regular people. Reality: As described above, QT’s effects on mortgage rates, savings yields, government borrowing costs, and financial market volatility all directly touch the finances of ordinary Americans — whether they invest in financial markets or not.

FAQ

Is quantitative tightening good or bad?

Neither universally. QT helps reduce inflation and rebuild the Fed’s policy tools — beneficial effects for the long-term health of the economy. But it also raises borrowing costs, tightens credit, and can create financial market volatility. Whether those costs are worth the benefits depends on current economic conditions and how carefully the Fed manages the process.

How does quantitative tightening affect my mortgage?

QT reduces the amount of money flowing into mortgage-backed securities, making mortgages more expensive to fund. This typically adds upward pressure to mortgage rates beyond what the federal funds rate alone would produce. Analysts estimate QT may contribute roughly 0.25–0.50 percentage points to long-term rates. Check current mortgage rates weekly at Freddie Mac’s Primary Mortgage Market Survey.

Is quantitative tightening the same as raising interest rates?

No. They’re separate tools. Rate hikes set the overnight borrowing cost between banks directly. QT reduces the overall supply of bank reserves gradually, tightening financial conditions through a different channel. The Fed can use one without the other, though it currently uses both simultaneously. Think of rates as the accelerator and QT as slowly draining the tank.

How long will quantitative tightening last?

The Fed has not specified an endpoint. It has said it will continue QT until reserves return to a level consistent with “ample” liquidity in the banking system — but economists disagree about where exactly that threshold is. The current pace of balance sheet reduction is expected to continue into 2027 at minimum, barring a recession or financial market disruption that forces the Fed to reverse course.

What happened the last time the Fed tried quantitative tightening?

The Fed conducted its first QT program from October 2017 to September 2019. It ended abruptly when market stress emerged in the short-term bank funding market in September 2019, forcing the Fed to resume adding reserves. That episode taught the Fed that it’s difficult to know in advance exactly when the balance sheet has shrunk enough — which is why it now monitors reserve levels closely and keeps its QT pace flexible.

Where can I track the Fed’s balance sheet?

The Federal Reserve publishes its balance sheet data weekly at the H.4.1 statistical release on the Fed’s website. The Federal Reserve Bank of St. Louis maintains a real-time chart at FRED — Federal Reserve Total Assets, updated weekly and free to access.

Conclusion: What You Should Take Away

Quantitative tightening is not something that happens only on Wall Street. It happens in your mortgage payment, your savings account yield, your stock portfolio’s volatility, and the federal government’s interest bill. It’s the Fed’s way of slowly withdrawing the extraordinary financial support it injected into the economy during the crisis years of 2008 and 2020 — and returning the financial system toward a more normal operating baseline.

What experts are watching in 2026 is whether the current QT program will end smoothly — with the balance sheet reaching a stable “ample reserves” endpoint — or whether it will need to be paused or reversed if financial conditions tighten too aggressively. The Fed has signaled it will adjust pace as needed.

What you should remember: QT is one of the most powerful but least-discussed tools in the Federal Reserve’s toolkit. Understanding how it works helps you understand why borrowing costs are elevated, why savings rates are higher than they were three years ago, and why the financial conditions you experience daily are shaped not just by the Fed’s interest rate decisions but by the size of its balance sheet.

© Fact and View, 2026. For informational purposes only. Not investment advice.

Be First to Comment