You’ve probably heard the phrase “Treasury yields rising” in news coverage of the economy, interest rates, or housing costs. But what exactly is a Treasury bond — and why should someone with no Wall Street background care about it?

The answer matters more than you might think. Treasury bonds influence the interest rate on your mortgage, your car loan, and your savings account. They fund government programs that millions of Americans rely on. And in 2026, with the national debt above $39 trillion and the Federal Reserve sending mixed signals about rate cuts, Treasury bonds are at the center of some of the most consequential economic debates in a generation.

This guide explains everything you need to know — from what a Treasury bond actually is to how you can buy one yourself — in plain English.

What Is a Treasury Bond?

A Treasury bond is a loan you make to the U.S. federal government.

Here’s the idea in everyday terms. When the government spends more than it collects in taxes, it needs to borrow the difference. It does that by selling bonds — essentially IOUs — to investors. You hand the government a set amount of money today. In return, the government promises to pay you regular interest payments over a fixed period, then return your original investment at the end.

The U.S. Treasury Department issues several types of these securities, but they all follow the same basic concept: lend money to the government, receive interest, get your money back at maturity.

A real-world example: Suppose you buy a 10-year Treasury bond with a face value of $1,000 and an annual interest rate — called a coupon rate — of 4.5%. The government pays you $45 every year for ten years. At the end of year ten, you receive your original $1,000 back. Your total return: $450 in interest plus your principal.

Types of Treasury Securities

The Treasury issues different products depending on how long the government wants to borrow for:

- Treasury bills (T-bills) — Short-term loans that mature in four weeks, three months, six months, or one year. Instead of regular interest payments, T-bills are sold at a discount: you pay $970 today and receive $1,000 when the bill matures.

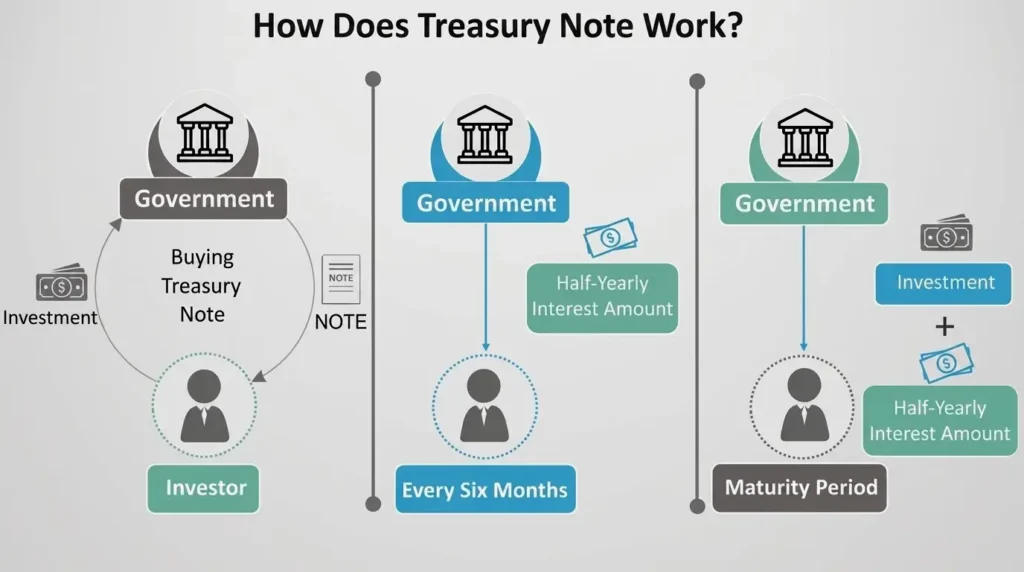

- Treasury notes (T-notes) — Medium-term loans that mature in two, three, five, seven, or ten years. Pay interest every six months.

- Treasury bonds (T-bonds) — Long-term loans that mature in twenty or thirty years. Also pay interest every six months.

- Treasury Inflation-Protected Securities (TIPS) — A special type of bond where the principal value rises with inflation, protecting your purchasing power.

- Series I Savings Bonds (I Bonds) — Government savings bonds available to individuals at TreasuryDirect.gov, with a return tied to the inflation rate.

When people refer to “Treasury yields” in news coverage, they’re usually talking about the interest rate on the 10-year Treasury note, which serves as a global benchmark for borrowing costs.

How the Interest Rate — and Yield — Works

Understanding the difference between a coupon rate and a yield confuses a lot of new investors. Here’s the key:

The coupon rate is fixed when the bond is issued. It doesn’t change. If you buy a $1,000 bond with a 4.5% coupon, you receive $45 per year for as long as you hold that bond.

The yield is different. It reflects what you actually earn based on the price you paid for the bond. And bonds are bought and sold on the open market after they’re issued, which means their prices fluctuate.

Here’s the core relationship every beginning investor should memorize:

When bond prices go up, yields go down. When bond prices go down, yields go up.

Think of it this way. If you paid $1,000 for a bond paying $45 per year, your yield is 4.5%. But if the price of that bond rises to $1,050 on the open market — because investors suddenly want more of them — and someone buys it there, they’re still only getting $45 per year, but now on an investment of $1,050. Their yield has dropped to about 4.3%.

This inverse relationship between bond prices and yields is one of the most fundamental mechanics in all of finance. It’s why you hear “bond yields fell” and “bond prices rallied” used interchangeably to describe the same event.

Related reading: Interest Rates Explained: How They Affect Your Money in 2026 — how the Treasury yield translates directly into your mortgage rate, auto loan, and savings account.

Why Treasury Bonds Matter to Ordinary Americans

You don’t have to own a single Treasury bond for them to affect your financial life. Here’s how:

Your mortgage rate is largely determined by the 10-year Treasury yield. Banks and lenders price home loans as a spread above that benchmark. When Treasury yields rise, mortgage rates follow. In 2026, the 10-year Treasury yield has held in the 4.3%–4.5% range, which is a key reason 30-year mortgage rates remain near 6.5%.

Your savings account is also connected. High Treasury yields give banks and online savings platforms a reason to compete for deposits by offering higher rates — which is why high-yield online savings accounts have been paying 4.5%–5% in 2026, compared to near-zero in 2021.

Your 401(k) and retirement funds typically hold some Treasury bonds as a stabilizing component. When stocks fall sharply, Treasury bonds often hold their value or rise in price — historically providing a cushion when equity markets decline.

Federal programs you rely on are partly funded by Treasury borrowing. Social Security, Medicare, military pay, and federal employee salaries all depend on the government’s ability to sell bonds to fund its spending when tax revenues fall short.

Related reading: US National Debt Explained: Should You Be Worried? — how the $39 trillion national debt and $1 trillion annual interest bill connect directly to Treasury market dynamics.

Benefits of Treasury Bonds

Safety: Treasury bonds are backed by the full faith and credit of the U.S. government. The U.S. has never defaulted on its debt. For investors who prioritize capital preservation over high returns, Treasuries are one of the safest investments in the world.

Predictable income: Because coupon payments are fixed, you know exactly what you’ll receive and when. This predictability makes Treasuries popular with retirees and anyone who needs reliable income from their investments.

Liquidity: The U.S. Treasury market is the largest and most liquid financial market in the world. You can buy or sell Treasury securities quickly and easily without significantly affecting the price.

Tax advantages: Interest earned on Treasury bonds is exempt from state and local income taxes — only federal tax applies. For investors in high-tax states like California or New York, this can make Treasuries more attractive than comparable corporate bonds.

Inflation protection with TIPS: If inflation is your primary concern, Treasury Inflation-Protected Securities adjust both principal and interest to match the Consumer Price Index, providing a guaranteed real (inflation-adjusted) return. In 2026, 10-year TIPS offer real yields of roughly 1.5%–2.0% — historically attractive by post-2008 standards.

Risks and Limitations

Interest rate risk: If you buy a 10-year Treasury bond today and yields rise next year, your bond is now worth less than you paid because newer bonds offer higher rates. If you sell before maturity, you’d receive less than face value. (If you hold to maturity, you receive exactly what was promised — this risk only applies to early sellers.)

Inflation risk: A standard (non-TIPS) Treasury bond pays a fixed coupon. If inflation rises faster than expected, the real purchasing power of those payments declines. A 4.5% coupon in an environment of 5% inflation means you’re losing ground in real terms.

Opportunity cost: Treasury bonds are safe, but they’re not growth investments. Over long periods, stocks have significantly outperformed bonds. Investors who park all their savings in Treasuries in their 30s or 40s may be sacrificing meaningful long-term wealth accumulation.

Fiscal risk (long-term): With U.S. national debt projected to reach 175% of GDP by 2056 per CBO projections, some economists argue that sustained Treasury supply at this scale will require permanently higher yields to attract buyers — meaning long-term bondholders face ongoing yield pressure, and the “safe” reputation of Treasuries depends on continued fiscal credibility.

Related reading: What Happens If US Debt Keeps Rising? — the fiscal context that shapes long-run Treasury market dynamics.

Common Misunderstandings

Myth: Treasury bonds and Treasury bills are the same thing. Reality: They’re all part of the same family of U.S. government debt securities, but they have very different maturities. T-bills mature in a year or less. T-notes mature in two to ten years. T-bonds mature in twenty to thirty years. The mechanics and price sensitivity to interest rate changes differ significantly between them.

Myth: When the Fed raises interest rates, your existing Treasury bond pays more. Reality: The coupon rate on an existing bond is fixed — it doesn’t change regardless of what the Fed does. What changes is the market price of your bond (which falls when rates rise) and the yield on newly issued bonds. Only new bonds issued after a rate increase will offer higher coupon rates.

Myth: You need a broker to buy Treasury bonds. Reality: You can purchase Treasury securities directly from the U.S. government at TreasuryDirect.gov, with no fees, no commissions, and no minimum purchase requirement beyond the standard $100 face value.

Myth: Treasury bonds are only for wealthy investors. Reality: Treasury securities are among the most accessible investments available to any American. I Bonds can be purchased for as little as $25. T-bills, T-notes, and T-bonds require a $100 minimum. Any working adult with a bank account can access them directly from the government.

Myth: If the U.S. goes bankrupt, you lose everything. Reality: The U.S. government cannot go bankrupt in the traditional sense — it issues the currency in which the debt is denominated. A more realistic concern is inflation eroding the purchasing power of your bond payments, not a formal default. TIPS specifically address this inflation risk.

How to Buy Treasury Bonds

You have three main options:

1. TreasuryDirect.gov — The official U.S. government portal. No fees. No intermediaries. You open a free account, link your bank, and purchase directly at auction. Best for individual investors who plan to hold to maturity.

2. Through a brokerage — Major brokers including Fidelity, Vanguard, Schwab, and Charles Schwab allow you to buy Treasuries at no commission, either at auction or on the secondary market. Easier to manage alongside other investments.

3. Through ETFs — Treasury ETFs like iShares 7-10 Year Treasury Bond ETF (IEF) or SPDR Portfolio Short Term Treasury ETF (SPTS) give you exposure to a basket of Treasury securities, with daily liquidity, no minimum holding period, and the ability to sell anytime during market hours.

FAQ

Are Treasury bonds a good investment in 2026?

It depends on your goals. Treasury bonds are not high-return growth investments, but they offer safety, predictable income, and portfolio stability. With the 10-year Treasury yield near 4.4% and inflation at 3.3%, the real return is modest but positive — more attractive than at any point from 2009 to 2022. They’re most appropriate for risk-averse investors, retirees, or anyone who wants a reliable income stream.

What happens to my Treasury bond if interest rates go up?

If you hold to maturity, nothing — you receive exactly what was promised (your coupon payments and face value). If you sell before maturity, your bond will be worth less on the market than you paid, because newer bonds now offer higher rates. This is called interest rate risk, and it’s the primary downside for short-term Treasury investors.

Is it better to buy I Bonds or regular Treasury bonds?

They serve different purposes. I Bonds adjust with inflation and are ideal for cash savings you want to preserve in purchasing power terms, up to the $10,000 annual limit. Regular Treasury notes and bonds offer fixed income at a known rate, greater liquidity (no 12-month minimum holding requirement), and no purchase limit. Most financial planners recommend considering both as part of a balanced savings strategy.

How much do Treasury bonds pay right now?

As of mid-2026, the 10-year Treasury note yields approximately 4.3%–4.5%, the 2-year Treasury yields roughly 3.8%–4.0%, and 30-year Treasury bonds yield approximately 4.7%–5.0%. I Bonds issued through April 2026 carry a composite yield of 4.03%. Track current yields daily at FRED — Federal Reserve Economic Data or TreasuryDirect.gov.

Can the U.S. government stop paying Treasury bonds?

The U.S. government has never defaulted on its Treasury bonds, and it has unique advantages that make a conventional default unlikely — it issues the currency in which the debt is owed. Occasional debt-ceiling political standoffs have raised short-term technical default concerns, but these have always resolved without a missed payment. A more realistic long-term risk is fiscal deterioration that eventually requires higher yields to attract buyers, rather than an outright payment failure.

Are Treasury bonds insured like bank deposits?

No — but they’re considered safer than FDIC-insured bank deposits in most practical respects. Treasury bonds are backed by the full faith and credit of the U.S. government, which prints the currency used to repay them. FDIC insurance protects bank deposits up to $250,000 per depositor per bank; Treasury bonds have no deposit limit and no insurance ceiling.

Where can I learn more about buying Treasury bonds?

TreasuryDirect.gov is the best starting point for purchasing I Bonds, T-bills, T-notes, and T-bonds directly from the U.S. government. Investopedia’s Treasury guide provides additional explainers, and the Federal Reserve’s consumer education page covers the relationship between Fed policy and Treasury yields in accessible terms.

Conclusion: What You Should Remember

Treasury bonds are one of the most important — and most misunderstood — financial instruments in the global economy.

They are the mechanism through which the U.S. government borrows money to fund everything from national defense to Social Security payments. They are the benchmark that determines what you pay on your mortgage and what you earn on your savings. And in 2026, with the national debt at a record, the Federal Reserve signaling possible rate hikes, and global appetite for U.S. debt attracting increased scrutiny from analysts and policymakers alike, they are more relevant to everyday Americans than at any point in recent memory.

You don’t need to be an economist to understand them. You don’t need a financial advisor to buy them. And you don’t need a large amount of money to get started.

What you do need is a basic grasp of how they work — and now you have one.

© Fact and View, 2026. For informational purposes only. Not investment advice. Always consult a qualified financial advisor before making investment decisions.

Be First to Comment