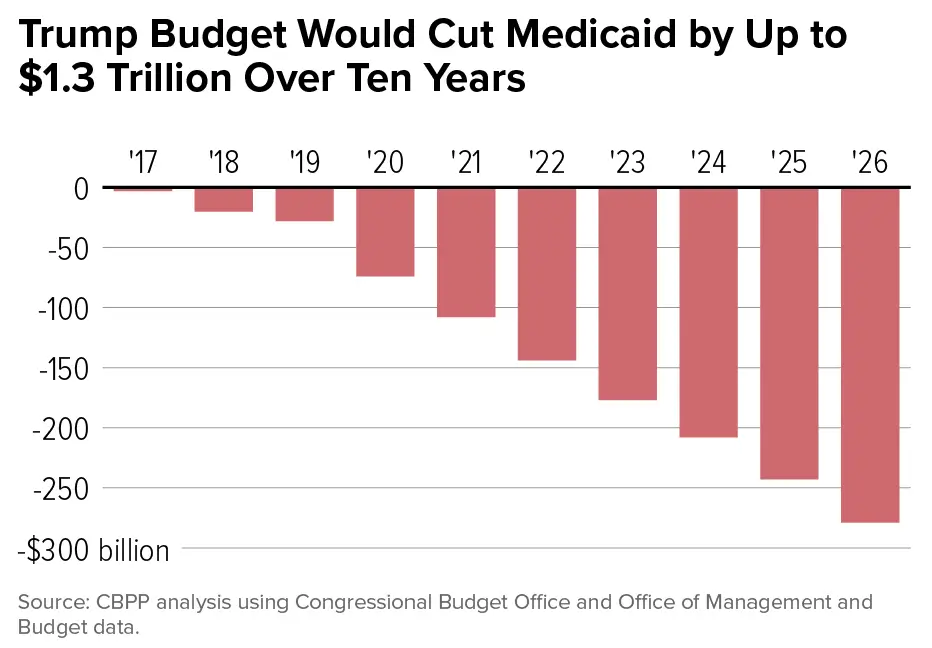

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act into law. Buried inside a 900-page legislative package that cut income taxes and reshaped the federal budget was a single provision that the American Medical Association called “the most sweeping and harmful Medicaid cuts in history.” The Congressional Budget Office’s estimate is specific: $1.02 trillion in Medicaid and CHIP federal spending cuts over ten years. 10.5 million people eliminated from the programs by 2034.

By 2026, the first wave of those changes is already in motion. The second wave — mandatory work requirements and semi-annual eligibility checks — activates in January 2027. The decisions being made in state capitals and federal agencies right now will determine which hospitals close, which patients lose coverage, and whether the rural communities most dependent on Medicaid funding survive the transition.

This is not a future risk. It is a present restructuring of the largest joint federal-state health insurance program in American history — one that covers 71 million Americans including children, pregnant women, elderly nursing home residents, and adults with disabilities.

The Big Picture: Why a $1 Trillion Cut, Why Now?

The OBBBA’s Medicaid cuts are not primarily a healthcare policy. They are a fiscal policy. The legislation required $3.3 trillion in deficit-financed tax cuts to be partially offset by spending reductions. Medicaid — as the largest discretionary-adjacent mandatory program with significant federal cost-sharing — was the largest available target.

Fact: CBO estimates the OBBBA will cut federal Medicaid and CHIP spending by $1.02 trillion over ten years through 2034. The three largest provisions by cost:

- Work requirements: $325–$326 billion in federal funding cuts, 2025–2034 — the largest single provision

- Provider tax limits: $191 billion in cuts from restricting state-directed provider tax mechanisms

- State-directed payment restrictions: $149 billion from limiting supplemental payment structures

Fact: The Urban Institute’s April 2026 analysis projects Medicaid enrollment decreasing by between 4.9 and 10.1 million people in 2028 alone from work requirements and more frequent eligibility checks — a range that reflects varying state implementation choices.

Fact: The Rural Health Transformation Program (RHTP) — a five-year, $50 billion program included in the OBBBA as a partial offset — distributed its first $10 billion across 50 states in 2026. This is the administration’s primary argument that rural healthcare access will be protected.

The View: The fiscal math of the OBBBA requires cuts of this magnitude to stay within budget reconciliation rules. Medicaid’s federal matching structure — where the federal government matches state spending at rates ranging from 50% to 90% — makes it the most direct lever for large-scale federal savings. The policy question is whether the healthcare delivery consequences of that fiscal decision are proportionate to the deficit savings achieved — and whether a $50 billion Rural Health Transformation Program adequately compensates for $1 trillion in cuts to a system those same rural communities depend on.

Related reading: Government Spending Explained: Where Your Tax Dollars Go — the full federal budget context showing how Medicaid’s $1 trillion in cuts fits into the broader fiscal architecture.

Deep Dive: Five Structural Changes and Their Consequences

1. Work Requirements: The Largest Single Coverage Reduction

The OBBBA’s mandatory work reporting requirement is the most consequential provision for coverage loss.

Fact: Beginning January 1, 2027 — with states able to implement earlier — adults aged 19–64 with incomes between 100% and 138% of the Federal Poverty Level must work, volunteer, or attend school for at least 80 hours per month to maintain Medicaid expansion eligibility.

Fact: CBO estimates work requirements will eliminate coverage for 5.3 million people by 2034. The Robert Wood Johnson Foundation’s March 2026 analysis projects between 4.9 and 10.1 million people losing Medicaid by 2028, depending on how aggressively states implement the requirements.

Fact: The Arkansas work requirement experiment — implemented and later struck down — provides direct empirical data. When Arkansas implemented similar requirements in 2018, approximately 18,000 people lost coverage within months. Many were workers whose shift patterns didn’t meet the reporting threshold, not unemployed people. Extrapolating that pattern nationally implies that a significant share of the 5.3 million projected to lose coverage under CBO’s estimate are already working — but will lose coverage due to administrative barriers, reporting complexity, or irregular work schedules.

The View: Work requirements are the most ideologically contested component of the Medicaid restructuring. Supporters argue that able-bodied working-age adults should demonstrate economic participation to receive taxpayer-funded benefits. Critics argue that the administrative architecture of work reporting — documentation requirements, monthly verification, digital literacy demands — creates barriers that eliminate coverage from working poor Americans rather than non-working ones. The Arkansas precedent is the most direct evidence available about how this plays out in practice.

2. Semi-Annual Eligibility Checks: The Administrative Coverage Erosion

Separate from work requirements, the OBBBA requires states to conduct Medicaid eligibility redeterminations every six months for expansion adults — doubling the current annual frequency.

Fact: CBO estimates the more frequent redetermination requirement will increase the number of uninsured by an additional 700,000 people by 2034 — on top of the 5.3 million from work requirements. Georgetown University’s Center for Children and Families projects the combined effect of work requirements and eligibility checks will produce 8.6 million newly uninsured by 2029, rising to 10 million by 2034.

States that expanded Medicaid under the ACA will bear the full impact of these requirements. Non-expansion states — where work requirements do not apply to the expansion population — face a narrower set of changes.

The View: More frequent redeterminations are a known coverage-erosion mechanism. The “churn” problem — eligible people cycling on and off coverage due to administrative requirements rather than eligibility changes — is well-documented in research on Medicaid administration. When states ran annual redeterminations after the COVID-era continuous enrollment requirement ended in 2023, approximately 20 million people were evaluated and millions lost coverage, many of whom were later found still eligible. The six-month cadence doubles the administrative surface area for coverage loss among people who remain eligible.

3. Provider Tax Limits: The State Fiscal Squeeze

Provider taxes — where states tax healthcare providers and use the revenue to qualify for higher federal Medicaid matching payments — fund a significant share of state Medicaid programs. The OBBBA restricts this mechanism beginning fiscal year 2027.

Fact: Beginning FY 2027, the OBBBA prohibits states from increasing healthcare provider taxes and restricts their use to qualify for federal matching payments. The CBO projects this provision will reduce federal Medicaid spending by $191 billion over ten years.

The fiscal consequence for states is direct: when states can no longer draw on provider tax revenue to match federal funds, they must either increase general fund contributions, cut provider payment rates, or reduce services. Research from the Center for American Progress shows that when federal Medicaid funding decreases, states tend to cut optional benefits first — including home- and community-based services (HCBS) for elderly and disabled populations.

4. Rural Hospital Exposure: The Most Acute Near-Term Risk

The intersection of work requirement coverage losses, provider tax restrictions, and provider payment rate pressures hits rural hospitals disproportionately.

Fact: Hundreds of labor and delivery units nationwide have already shut their doors due to budget shortfalls in recent years, per the National Health Law Program’s September 2025 analysis. Particularly in rural communities, people must drive hours to access pregnancy-related care.

Fact: The OBBBA’s Rural Health Transformation Program provides $50 billion over five years — $10 billion for 2026. HFMA’s March 2026 state-by-state analysis found that some rural states with limited provider tax exposure (Nebraska, North Dakota) may break even. Non-expansion states like Wyoming and Alabama face minimal impact from work requirements, and Wyoming could see a budget increase of more than 10% from RHTP inflows. But rural hospitals in expansion states — which depend on Medicaid expansion payments for financial viability — face the compounded pressure of coverage losses, provider tax restrictions, and payment rate reductions simultaneously.

The View: The RHTP is the most credible element of the administration’s argument that rural healthcare access will be protected. The problem is scale: $50 billion over five years against $1 trillion in Medicaid cuts over ten years represents a 5-cent offset on every dollar removed. For a rural hospital that derives 40% of its revenue from Medicaid, a 15–20% reduction in Medicaid enrollment in its service area is an existential financial threat that RHTP funds do not proportionally address.

5. The Young Adult Coverage Gap

The OBBBA’s healthcare provisions create a specific structural vulnerability for young adults — already the most uninsured age group in America.

Fact: Young adults have the highest uninsurance rate of any age group — approximately 11% — and the lowest rates of employer-provided health insurance. The Urban Institute’s August 2025 analysis found that Medicaid cuts leave 3 in 10 young adults vulnerable to losing health care access.

Fact: Starting January 2026, the OBBBA eliminated enhanced federal funding for states choosing to expand Medicaid for the first time — removing the primary financial incentive for the remaining non-expansion states to cover their uninsured adult populations.

Fact: Work requirements will disproportionately affect young adults aged 19–35 in low-wage, irregular-schedule employment — gig workers, hospitality workers, retail employees — whose work patterns are hardest to document on monthly reporting systems.

Related reading: Why Millennials Can’t Afford Homes — the housing and healthcare cost squeeze converging on the same demographic simultaneously.

Risks & Opportunities: Three Scenarios

Base Case (~50% probability): Partial Implementation, State Variation

Work requirements activate January 2027. Coverage losses reach 3–5 million by end of 2027, concentrated in expansion states with aggressive implementation. State fiscal pressure forces provider payment rate cuts. Rural hospitals in high-exposure states begin closure announcements by late 2026. RHTP funds partially offset losses in low-exposure rural states.

What this means for you: If you are currently enrolled in Medicaid expansion, determine your state’s implementation timeline. Most states must implement by January 2027. Work requirement documentation requirements will be complex — 80 hours/month with monthly verification. Start documenting now.

Upside Scenario (~20% probability): Legal Challenges Delay Implementation

Multiple state and federal lawsuits challenge work requirements as violating Medicaid’s statutory purpose. Federal courts issue preliminary injunctions, delaying implementation beyond January 2027. Coverage losses are smaller in scale. States gain negotiating leverage to modify implementation. Arkansas precedent of judicial reversal repeats at national scale.

What this means for you: Legal uncertainty about work requirements extends through 2027. Track litigation developments at National Health Law Program. Coverage may remain intact for longer than current implementation timelines suggest.

Downside Scenario (~30% probability): Accelerated Coverage Loss, Hospital Closures

Aggressive state implementation by mid-2026 in 10+ expansion states. Coverage losses reach 7–10 million by 2028, within CBPP’s projected range of 9.9–14.9 million at risk. Rural hospital closures accelerate. Provider payment rate reductions reduce Medicaid-accepting physician supply. Emergency room utilization spikes as displaced patients lose primary care access.

What this means for you: Emergency room care becomes the default for millions of uninsured patients who previously had Medicaid coverage. ER costs — the most expensive healthcare delivery method — shift to hospital uncompensated care budgets, increasing pressure on all payers including private insurers. Hospital system consolidation accelerates as smaller rural facilities close, reducing competition and raising prices in surviving markets.

Related reading: New US Laws in 2026: What They Mean for Americans — the full OBBBA provisions affecting Medicaid, SNAP, and healthcare simultaneously.

The Bottom Line

The Medicaid restructuring contained in the OBBBA is the largest single change to American healthcare coverage since the ACA’s passage in 2010 — and unlike the ACA, it reduces coverage rather than expanding it. Whether it constitutes reform or risk depends on which analysis you weight and which population you prioritize.

For current Medicaid enrollees:

- Determine your state’s OBBBA implementation timeline — available at your state Medicaid office or Medicaid.gov

- If you are in a Medicaid expansion state, work requirements activate January 1, 2027 for most states

- Begin documenting employment hours, volunteer activity, or school enrollment now — 80 hours/month minimum

- Explore ACA marketplace plans as a fallback; use the HealthCare.gov premium estimator to compare costs

For healthcare providers and hospitals:

- Rural hospitals in expansion states should model the financial impact of 15–25% Medicaid enrollment reductions in their service areas

- Provider tax restriction begins FY 2027 — audit current provider tax revenue contribution to your Medicaid matching claims

- RHTP funds ($10B in 2026, $50B over five years) are available — ensure your facility has filed for allocation

For investors and business owners:

- Hospital and managed care equities face significant earnings uncertainty from coverage loss at this scale

- Home health, behavioral health, and dental services — heavily dependent on Medicaid’s optional benefit funding — face above-average revenue risk

- States with high Medicaid expansion enrollment in their workforce populations may see labor market tightening as uninsured workers face healthcare cost pressure that reduces employment flexibility

The $1 trillion in Medicaid cuts produces real federal savings against a $39 trillion national debt and a $1.9 trillion annual deficit. Whether those savings are worth the coverage loss, hospital closures, and healthcare access reduction they will produce is the central healthcare policy question of the 2026 midterm cycle.

FAQ

How much is the OBBBA cutting from Medicaid?

The Congressional Budget Office estimates the OBBBA cuts federal Medicaid and CHIP spending by $1.02 trillion over 10 years through 2034. The three largest provisions are: work requirements ($325–$326 billion), provider tax limits ($191 billion), and state-directed payment restrictions ($149 billion). These are the largest Medicaid cuts in the program’s 60-year history. Read the official CBO analysis at cbo.gov and Georgetown CCF’s coverage tracking at ccf.georgetown.edu.

How many people will lose Medicaid coverage?

CBO projects that 10 to 10.5 million people will lose Medicaid or CHIP coverage by 2034, with 7.5 million becoming uninsured from Medicaid-specific cuts. By year: 1.3 million newly uninsured in 2026, rising to 5.2 million in 2027, 6.8 million in 2028, and 10 million by 2034. The CBPP projects a wider range of 9.9–14.9 million at risk of losing coverage. The RWJF’s March 2026 analysis projects 4.9–10.1 million losing coverage in 2028 from work requirements and eligibility checks alone, with the range reflecting state implementation choices.

What are Medicaid work requirements and when do they start?

Work requirements mandate that Medicaid expansion adults aged 19–64 with incomes between 100% and 138% of the Federal Poverty Level must work, volunteer, or attend school for at least 80 hours per month to maintain eligibility. They begin January 1, 2027, for most states — though states may implement earlier. Monthly documentation and verification is required. CBO projects 5.3 million people will lose coverage specifically from this provision by 2034. The Arkansas 2018 work requirement experiment is the closest empirical precedent — 18,000 people lost coverage in months, many of whom were working but failed to meet documentation requirements.

Which states are most affected by Medicaid cuts?

Medicaid expansion states — the 40 states that expanded coverage to adults with incomes at or below 138% of the Federal Poverty Level — bear the largest impact from work requirements, more frequent eligibility checks, and provider tax restrictions. HFMA’s March 2026 analysis identified expansion states with significant provider-tax programs and state-directed payment structures as most exposed. Rural expansion states — where hospitals depend heavily on Medicaid for financial viability — face the highest risk of provider closures. Non-expansion states like Wyoming and Alabama face minimal work requirement impact and may see net budget increases from the Rural Health Transformation Program’s $50 billion over five years.

What is the Rural Health Transformation Program and will it protect rural hospitals?

The RHTP is a five-year, $50 billion program included in the OBBBA to help rural healthcare providers navigate the transition. It distributed its first $10 billion across all 50 states in 2026. For states with minimal provider tax exposure and no Medicaid expansion, RHTP funds may exceed Medicaid losses — Wyoming, for example, could see a net budget increase. For rural expansion states where hospitals derive 30–50% of revenue from Medicaid patients, the RHTP provides partial but insufficient compensation for $1 trillion in federal cuts. The scale mismatch — $50 billion offset against $1 trillion in cuts — is the central criticism of the program from healthcare provider groups.

What should I do if I have Medicaid coverage?

Three immediate steps for current Medicaid enrollees:

- Check your state’s implementation timeline — contact your state Medicaid office or visit Medicaid.gov to find your state’s OBBBA implementation schedule

- Document your work activity now — begin tracking hours worked, volunteer activities, or school enrollment with documentation that can be submitted for verification; 80 hours/month is the minimum threshold

- Understand your marketplace options — if you lose Medicaid eligibility, you qualify for a Special Enrollment Period to purchase ACA marketplace insurance. Use the HealthCare.gov plan finder to model premium costs before coverage loss occurs

Sources: CBO — OBBBA Health Coverage Estimates, August 2025 · RWJF — Millions Could Lose Medicaid Coverage, March 2026 · CBPP — By the Numbers: Harmful Republican Megabill, August 2025 · AMA — Changes to Medicaid and OBBBA, June 2026 · Urban Institute — 3 in 10 Young Adults Vulnerable, August 2025 · Center for American Progress — Truth About OBBBA Cuts, August 2025 · HFMA — OBBBA Medicaid Cuts and State Budget Impact, March 2026 · National Health Law Program — Work Requirements and Reproductive Health, September 2025 · SNAP Eligibility Calculator — OBBBA Impact Summary

© Fact and View, 2026. For informational purposes only. Not legal or medical advice. Consult a qualified professional for guidance specific to your situation.

Be First to Comment